Creating different forecast paths for forecast objects (when applicable),

by utilizing the underlying model distribution with the simulate function.

Usage

ts_forecast_simulator(

.model,

.data,

.ext_reg = NULL,

.frequency = NULL,

.bootstrap = TRUE,

.horizon = 4,

.iterations = 25,

.sim_color = "steelblue",

.alpha = 0.05

)Arguments

- .model

A forecasting model of one of the following from the

forecastpackage:Arima()with xreg

- .data

The data that is used for the

.modelparameter. This is used withtimetk::tk_index()- .ext_reg

A

tibbleormatrixof future xregs that should be the same length as the horizon you want to forecast.- .frequency

This is for the conversion of an internal table and should match the time frequency of the data.

- .bootstrap

A boolean value of TRUE/FALSE. From

forecast::simulate.Arima()Do simulation using resampled errors rather than normally distributed errors.- .horizon

An integer defining the forecast horizon.

- .iterations

An integer, set the number of iterations of the simulation.

- .sim_color

Set the color of the simulation paths lines.

- .alpha

Set the opacity level of the simulation path lines.

Details

This function expects to take in a model of either Arima,

auto.arima, ets or nnetar from the forecast package. You can supply a

forecasting horizon, iterations and a few other items. You may also specify

an Arima() model using xregs.

See also

Other Simulator:

ts_arima_simulator()

Examples

suppressPackageStartupMessages(library(forecast))

suppressPackageStartupMessages(library(dplyr))

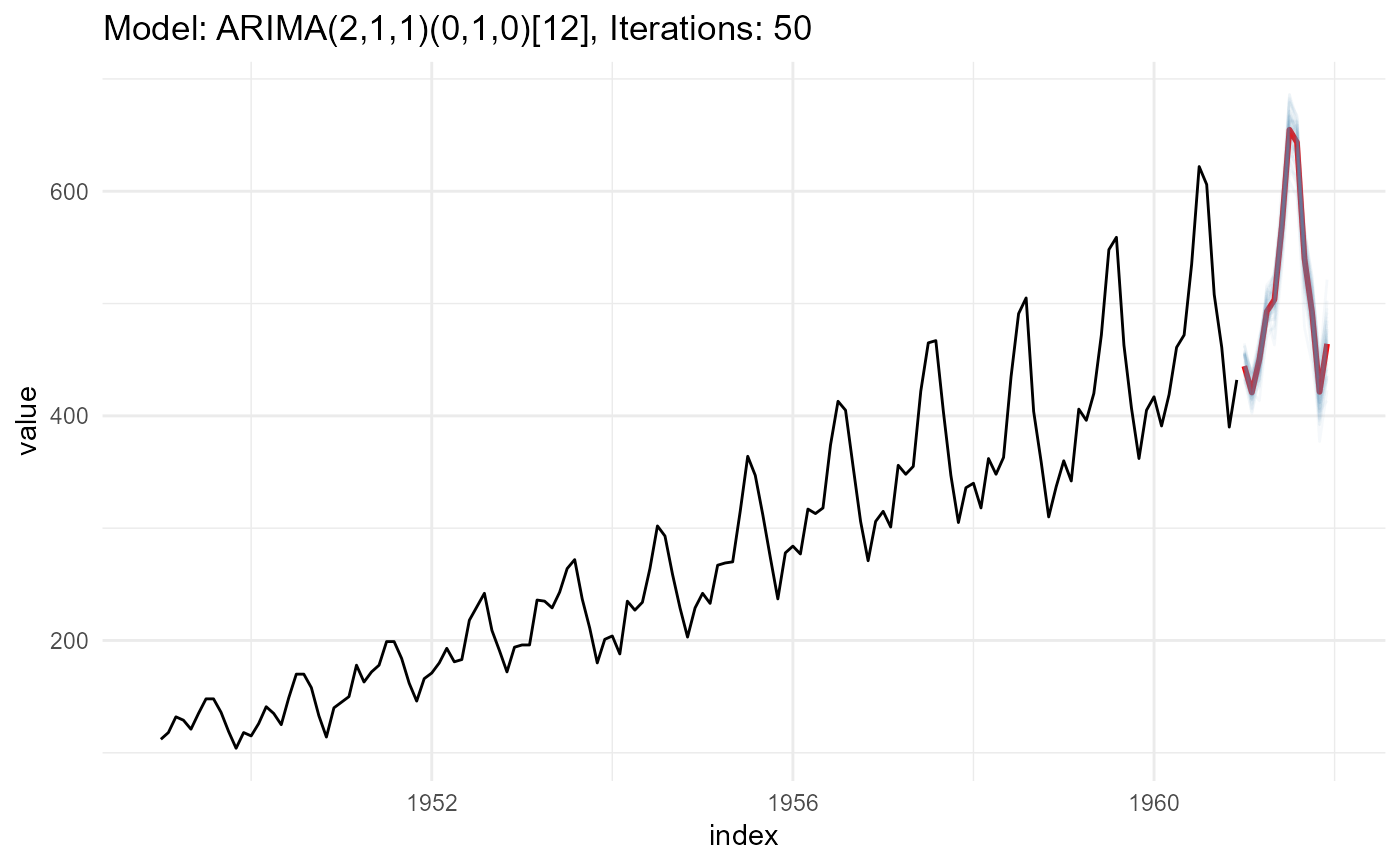

# Create a model

fit <- auto.arima(AirPassengers)

data_tbl <- ts_to_tbl(AirPassengers)

# Simulate 50 possible forecast paths, with .horizon of 12 months

output <- ts_forecast_simulator(

.model = fit

, .horizon = 12

, .iterations = 50

, .data = data_tbl

)

output$ggplot