Continuous Distribution Generators

Source:vignettes/continuous-distribution-generators.Rmd

continuous-distribution-generators.RmdRandomWalker provides a comprehensive suite of random walk generators based on continuous probability distributions. Each function follows a consistent API design for ease of use.

Table of Contents

- Common Parameters

- Normal Distribution

- Brownian Motion

- Geometric Brownian Motion

- Beta Distribution

- Cauchy Distribution

- Chi-Squared Distribution

- Exponential Distribution

- F Distribution

- Gamma Distribution

- Log-Normal Distribution

- Logistic Distribution

- Student’s t Distribution

- Uniform Distribution

- Weibull Distribution

- Comparison Guide

Common Parameters

All continuous distribution generators share these common parameters:

| Parameter | Type | Description | Default |

|---|---|---|---|

.num_walks |

Integer | Number of walks to generate | 25 |

.n |

Integer | Number of steps per walk | 100 |

.initial_value |

Numeric | Starting value for the walk | 0 |

.dimensions |

Integer | Spatial dimensions (1, 2, or 3) | 1 |

Additional parameters are distribution-specific and control the shape of the probability distribution.

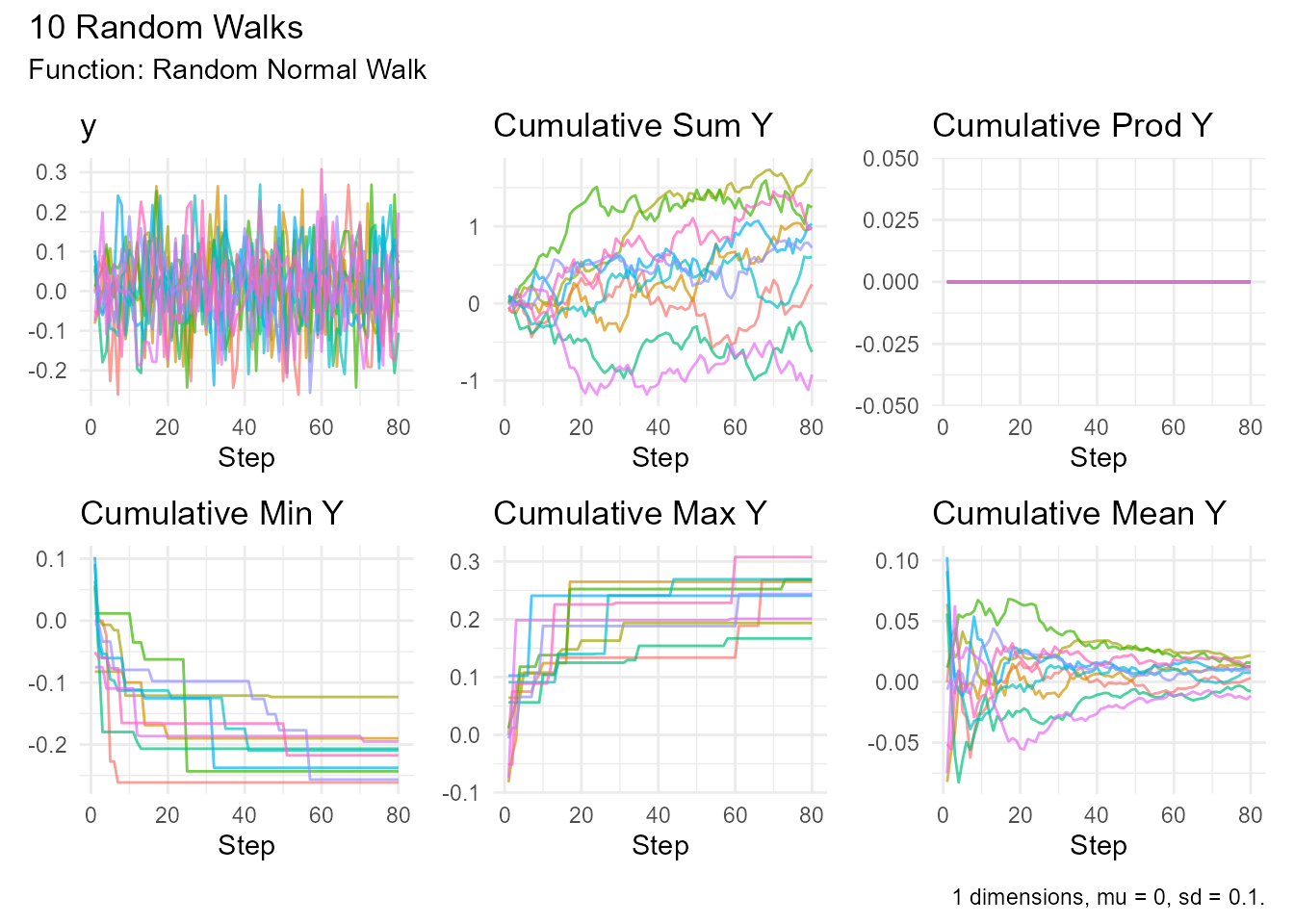

Normal Distribution

random_normal_walk()

The most commonly used random walk, based on the normal (Gaussian) distribution.

Function Signature:

random_normal_walk(

.num_walks = 25,

.n = 100,

.mu = 0,

.sd = 1,

.initial_value = 0,

.dimensions = 1

)Distribution Parameters: - .mu - Mean

of the distribution (default: 0) - .sd - Standard deviation

(default: 1)

Use Cases: - General-purpose random walks - Modeling measurement errors - Simulating natural phenomena with normal noise

Example:

# Basic normal walk

random_normal_walk(.num_walks = 10, .n = 100) |>

visualize_walks()

# With custom mean and SD

random_normal_walk(

.num_walks = 5,

.n = 200,

.mu = 0.01, # Slight upward drift

.sd = 0.5, # Lower volatility

.initial_value = 100

) |> visualize_walks()

# 2D spatial walk

random_normal_walk(

.num_walks = 3,

.n = 500,

.dimensions = 2

) |> visualize_walks()

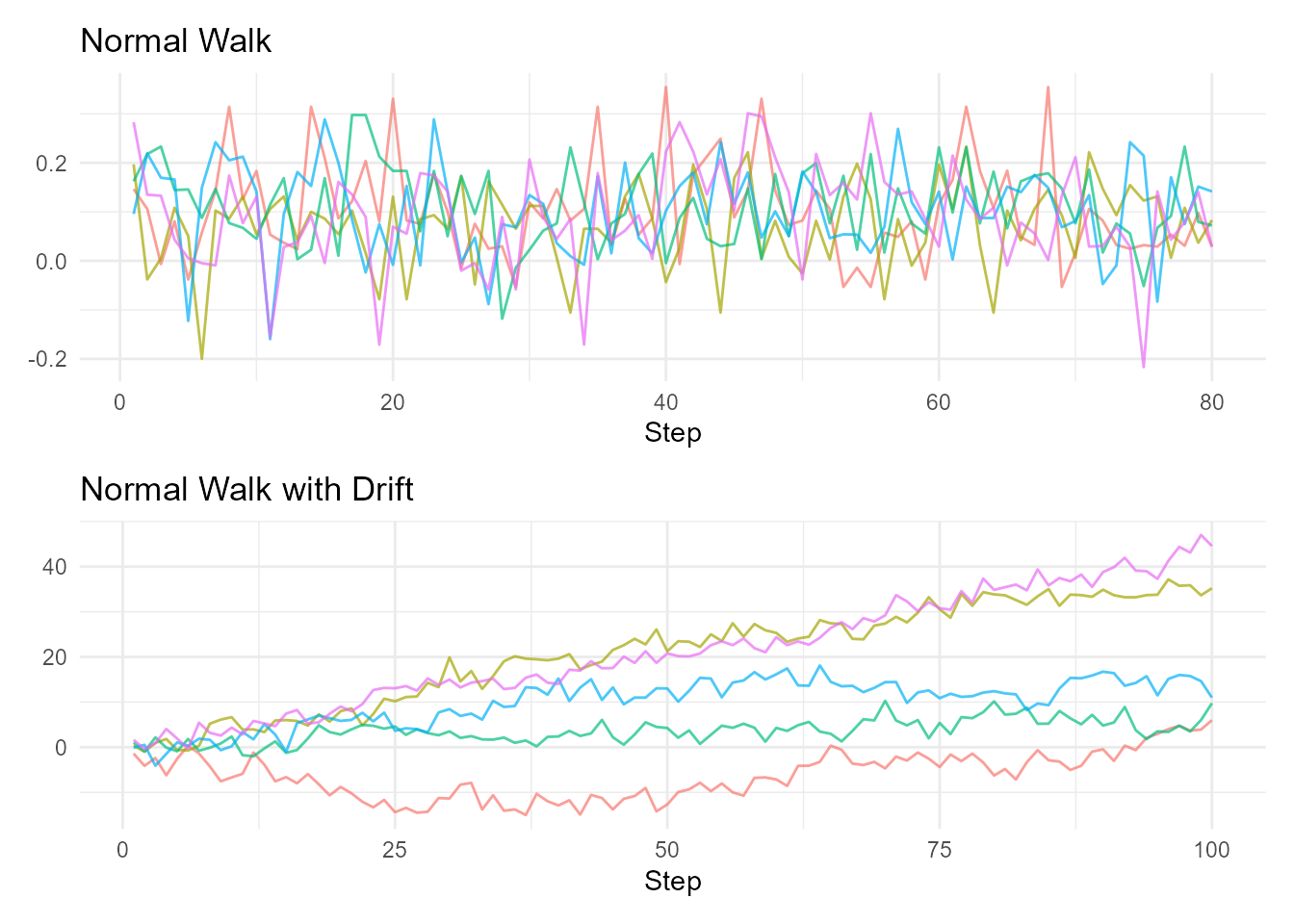

random_normal_drift_walk()

Random walk with deterministic drift component.

Function Signature:

random_normal_drift_walk(

.num_walks = 25,

.n = 100,

.mu = 0,

.sd = 1,

.initial_value = 0,

.dimensions = 1

)Key Difference from

random_normal_walk(): - .drift -

Drift term added to each step (default: 0.1) - Adds explicit drift term:

drift + random_step - More pronounced trending behavior -

Better for modeling processes with clear directional movement

Example:

# Compare walks with and without drift

p1 <- random_normal_walk(.num_walks = 5, .mu = 0.1) |>

visualize_walks(.pluck = "y") +

labs(title = "Normal Walk")

p2 <- random_normal_drift_walk(.num_walks = 5, .mu = 0.1) |>

visualize_walks(.pluck = "y") +

labs(title = "Normal Walk with Drift")

p1 / p2

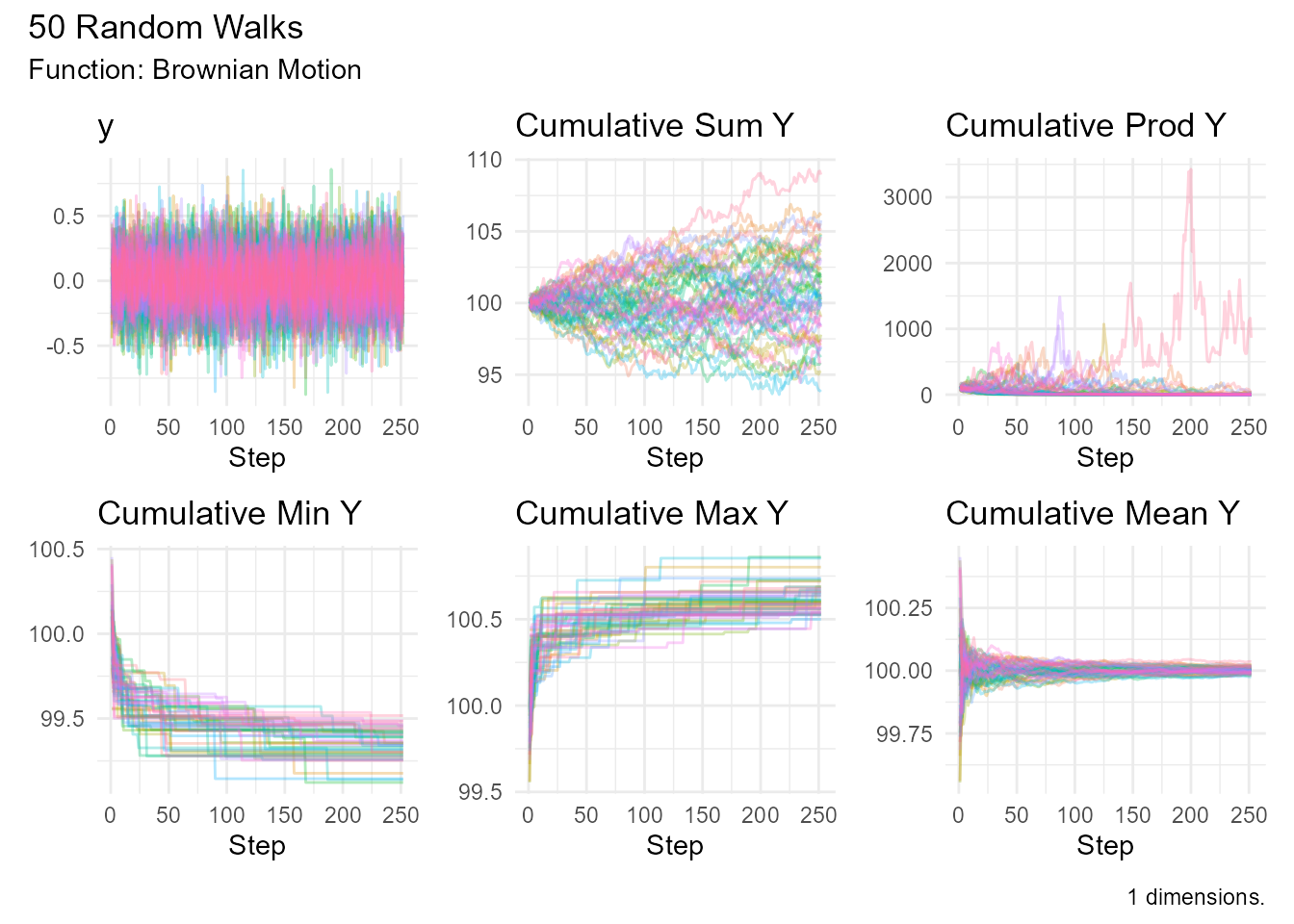

Brownian Motion

brownian_motion()

Standard Brownian motion (Wiener process) - the foundation of stochastic calculus.

Function Signature:

brownian_motion(

.num_walks = 25,

.n = 100,

.delta_time = 1,

.initial_value = 0,

.dimensions = 1

)Parameters: - .num_walks - Number of

walks to generate (default: 25) - .n - Number of steps per

walk (default: 100) - .delta_time - Time increment per step

(default: 1) - .initial_value - Starting value for each

walk (default: 0) - .dimensions - Number of dimensions

(default: 1)

Mathematical Form:

Use Cases: - Financial mathematics (Black-Scholes model) - Physics (particle diffusion) - Signal processing (noise modeling)

Example:

# Standard Brownian motion

brownian_motion(.num_walks = 10) |>

visualize_walks()

# With drift and volatility

brownian_motion(

.num_walks = 50,

.n = 252,

.delta_time = 0.05,

.initial_value = 100

) |> visualize_walks(.alpha = 0.3)

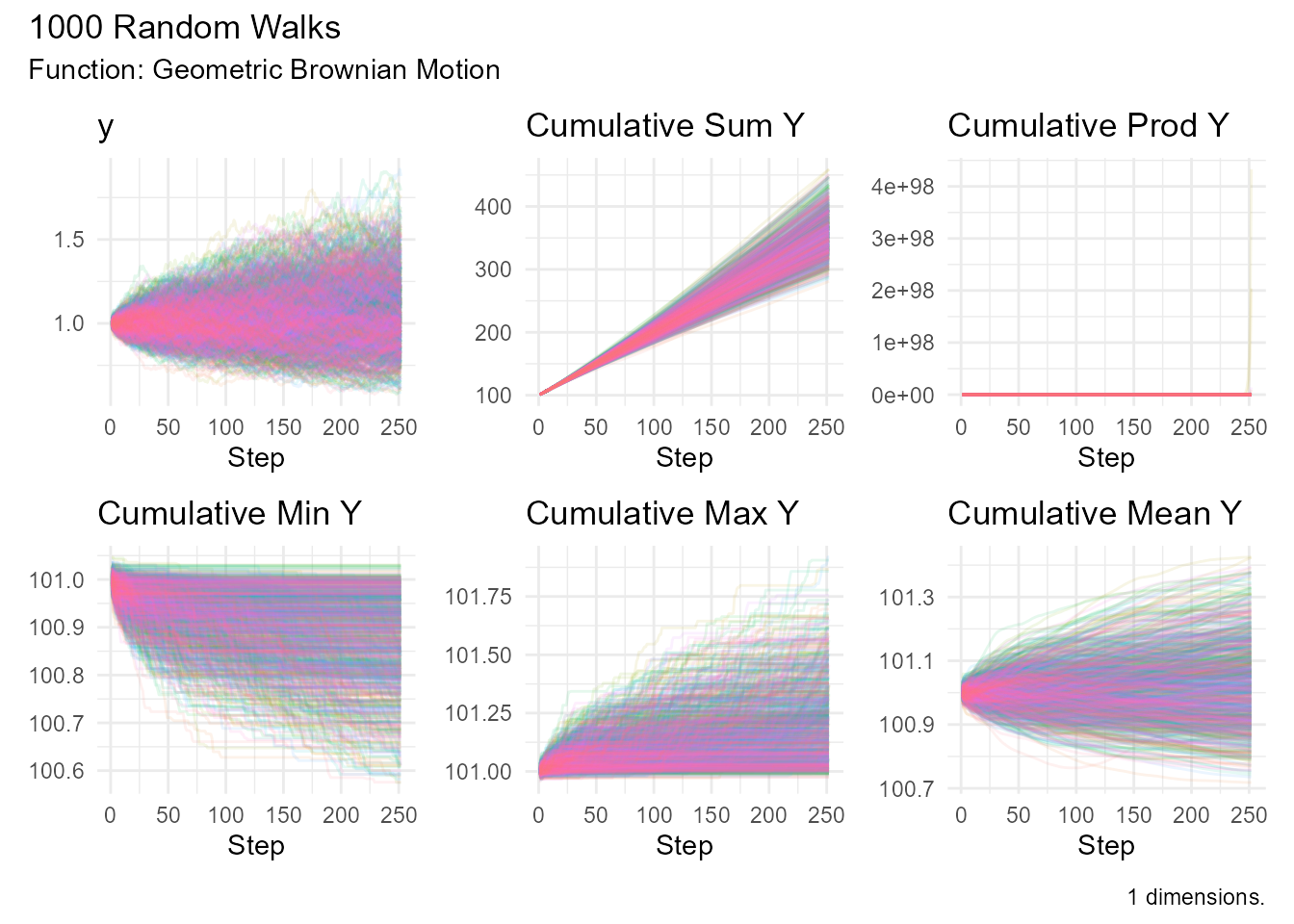

geometric_brownian_motion()

Geometric Brownian motion - the standard model for stock prices.

Function Signature:

geometric_brownian_motion(

.num_walks = 25,

.n = 100,

.mu = 0,

.sigma = 0.1,

.initial_value = 100,

.delta_time = 0.003,

.dimensions = 1

)Parameters: - .mu - Expected return

(drift) - .sigma - Volatility

Mathematical Form:

dS(t) = μ S(t) dt + σ S(t) dW(t)

S(t) = S(0) exp((μ - σ²/2)t + σW(t))Key Properties: - Always positive (can’t go below zero) - Log-normal distribution of prices - Percentage changes are normally distributed

Use Cases: - Stock price modeling - Option pricing - Asset allocation simulations - Monte Carlo risk analysis

Example:

# Model stock prices

stock_sim <- geometric_brownian_motion(

.num_walks = 1000,

.n = 252, # Trading days in a year

.mu = 0.08, # 8% expected return

.sigma = 0.25, # 25% volatility

.initial_value = 100

)

# Visualize scenarios

stock_sim |> visualize_walks(.alpha = 0.1)

# Analyze outcomes

stock_sim |>

summarize_walks(.value = cum_prod_y, .group_var = walk_number) |>

summarize(

median_price = median(max_val),

prob_profit = mean(max_val > 100),

prob_loss_50 = mean(min_val < 50)

)Beta Distribution

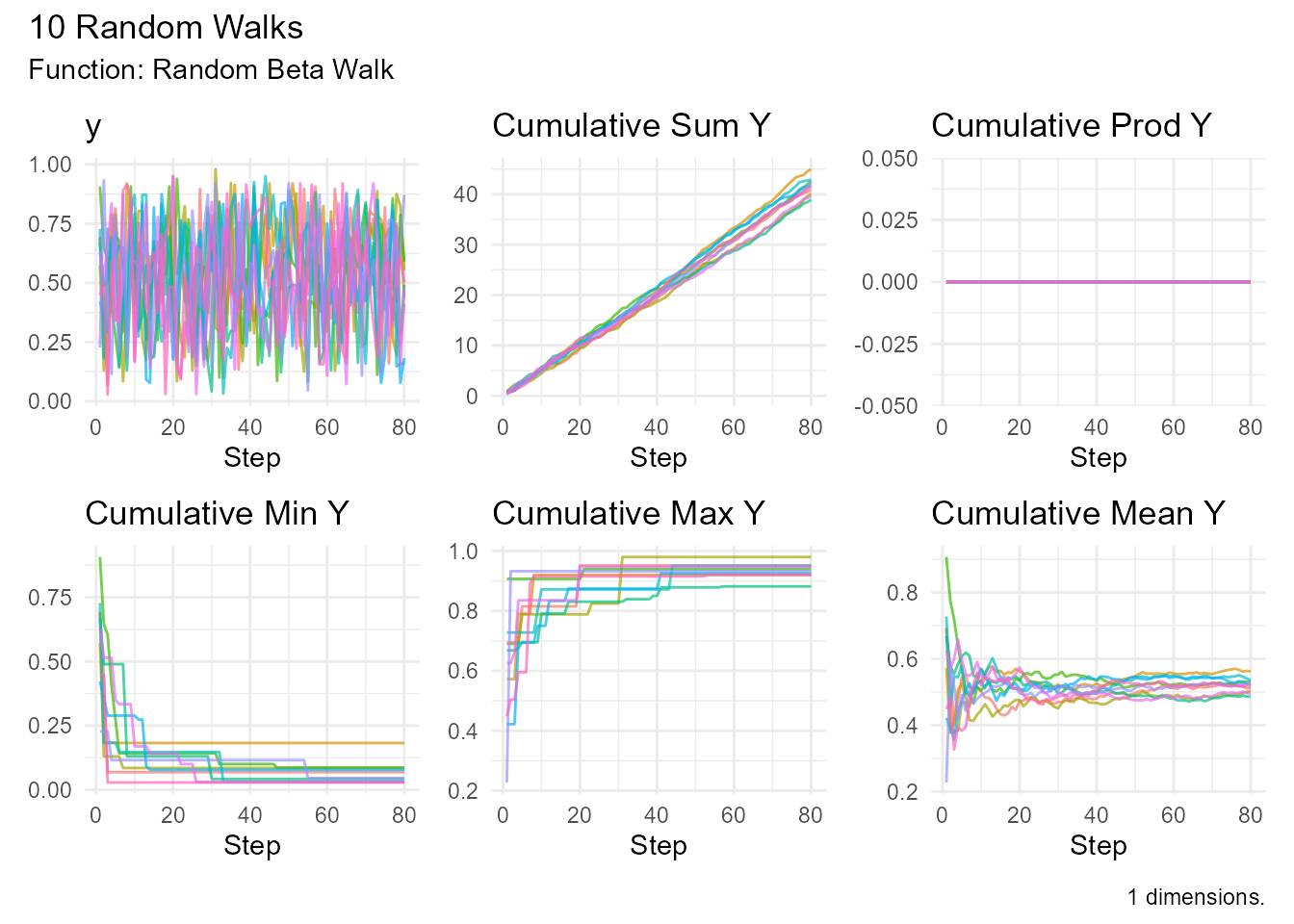

random_beta_walk()

Random walk based on the beta distribution (bounded between 0 and 1).

Function Signature:

random_beta_walk(

.num_walks = 25,

.n = 100,

.shape1 = 2,

.shape2 = 2,

.ncp = 0,

.initial_value = 0,

.samp = TRUE,

.replace = TRUE,

.sample_size = 0.8,

.dimensions = 1

)Parameters: - .shape1 - First shape

parameter (α) - .shape2 - Second shape parameter (β) -

.ncp - Non-centrality parameter (default: 0)

Properties: - Steps are bounded: 0 ≤ step ≤ 1 - Flexible shapes (uniform, U-shaped, bell-shaped) - Mean = α / (α + β) - Variance = (α β) / ((α + β)² (α + β + 1))

Shape Guide: - shape1 = 1, shape2 = 1:

Uniform (0,1) - shape1 = 2, shape2 = 2: Symmetric,

bell-shaped - shape1 = 2, shape2 = 5: Right-skewed -

shape1 = 5, shape2 = 2: Left-skewed

Use Cases: - Modeling proportions or percentages - Bounded processes (e.g., utilization rates) - Success rates over time

Example:

# Symmetric beta walk

random_beta_walk(

.num_walks = 10,

.shape1 = 2,

.shape2 = 2

) |> visualize_walks()

# Right-skewed (toward 0)

random_beta_walk(

.num_walks = 10,

.shape1 = 2,

.shape2 = 5

) |> visualize_walks()

# Compare different shapes

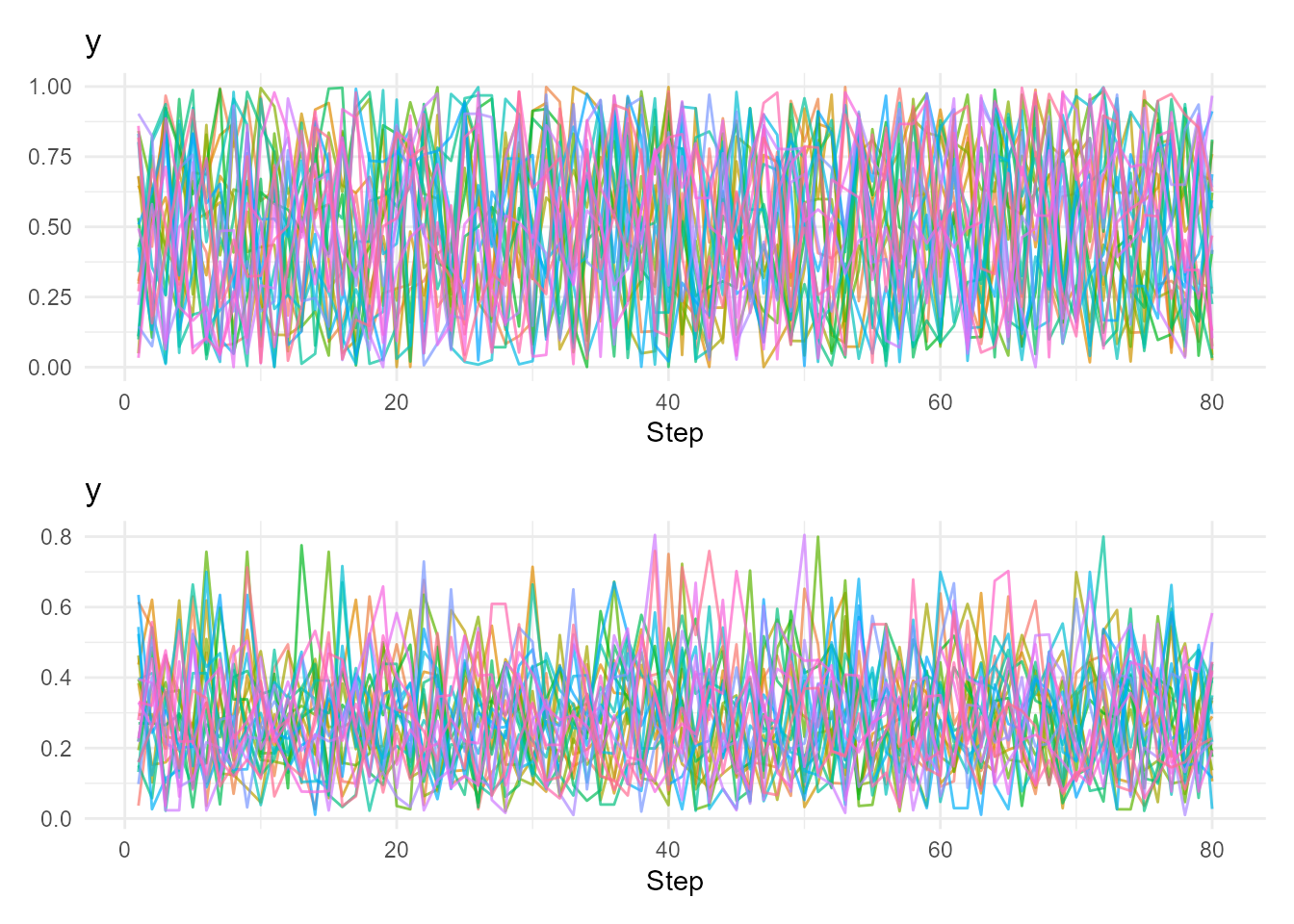

p1 <- random_beta_walk(.shape1 = 1, .shape2 = 1) |>

visualize_walks(.pluck = "y")

p2 <- random_beta_walk(.shape1 = 2, .shape2 = 5) |>

visualize_walks(.pluck = "y")

p1 / p2

Cauchy Distribution

random_cauchy_walk()

Random walk with heavy tails - extreme values are much more common than in normal distribution.

Function Signature:

random_cauchy_walk(

.num_walks = 25,

.n = 100,

.location = 0,

.scale = 1,

.initial_value = 0,

.samp = TRUE,

.replace = TRUE,

.sample_size = 0.8,

.dimensions = 1

)Parameters: - .location - Location

parameter (median) - .scale - Scale parameter (spread)

Properties: - No defined mean or variance! - Heavy tails (high probability of extreme values) - Symmetric around location - Much more volatile than normal distribution

Use Cases: - Modeling extreme events - Financial crises simulation - Physics (resonance phenomena) - Robust statistics demonstrations

Example:

# Standard Cauchy walk

random_cauchy_walk(.num_walks = 10) |>

visualize_walks()

# Compare with normal walk

p1 <- random_normal_walk(.num_walks = 5, .sd = 1) |>

visualize_walks(.pluck = "y") +

labs(title = "Normal Walk")

p2 <- random_cauchy_walk(.num_walks = 5, .scale = 1) |>

visualize_walks(.pluck = "y") +

labs(title = "Cauchy Walk (Heavy Tails)")

p1 / p2

Chi-Squared Distribution

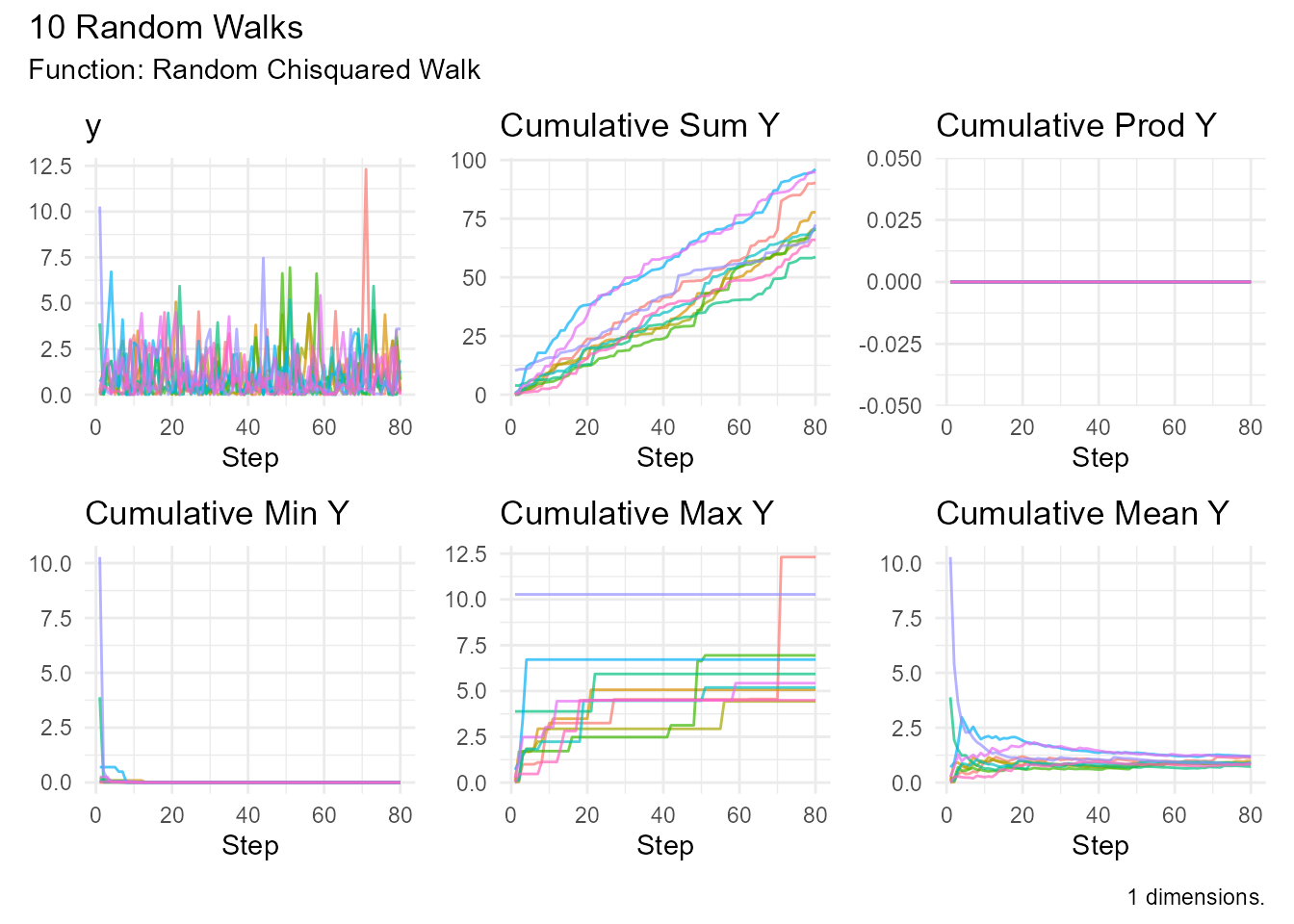

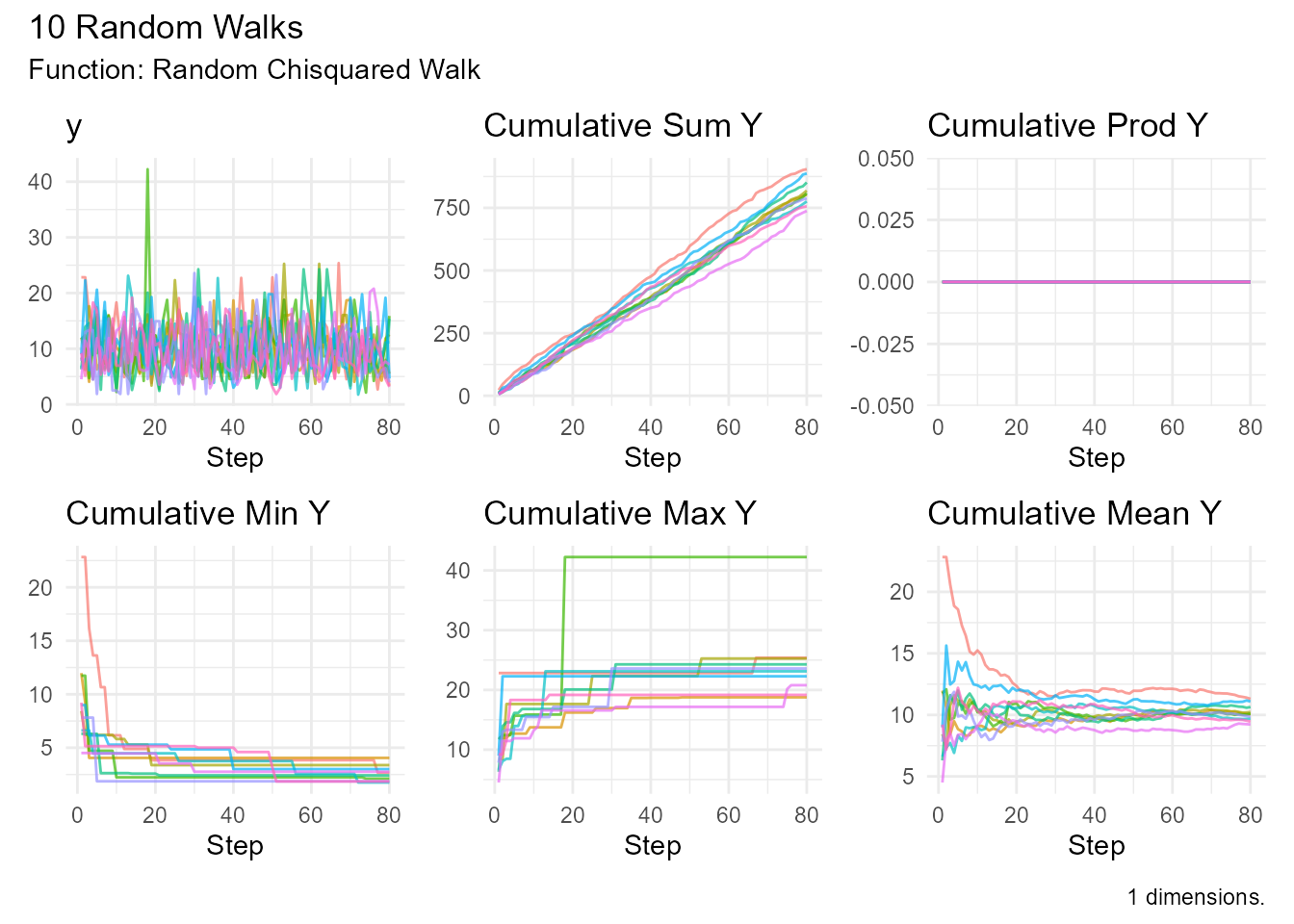

random_chisquared_walk()

Random walk based on chi-squared distribution (always positive).

Function Signature:

random_chisquared_walk(

.num_walks = 25,

.n = 100,

.df = 5,

.ncp = 0,

.initial_value = 0,

.samp = TRUE,

.replace = TRUE,

.sample_size = 0.8,

.dimensions = 1

)Parameters: - .df - Degrees of freedom

- .ncp - Non-centrality parameter (default: 0)

Properties: - Steps are always positive - Right-skewed (especially for low df) - Mean = df - Variance = 2df

Use Cases: - Goodness-of-fit tests - Variance estimation - Quality control - Reliability engineering

Example:

# Low df (very skewed)

random_chisquared_walk(.num_walks = 10, .df = 1) |>

visualize_walks()

# Higher df (more symmetric)

random_chisquared_walk(.num_walks = 10, .df = 10) |>

visualize_walks()

Exponential Distribution

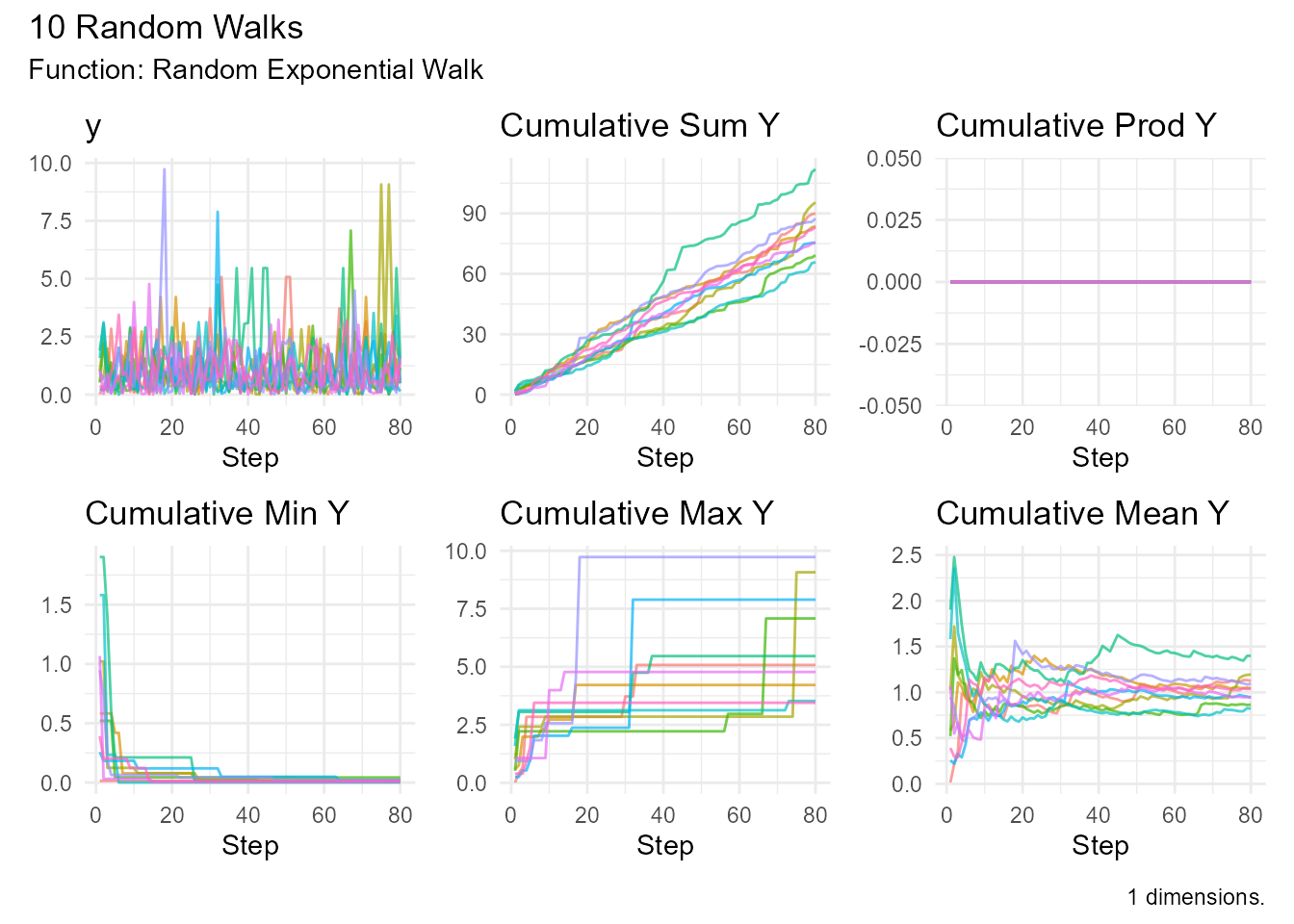

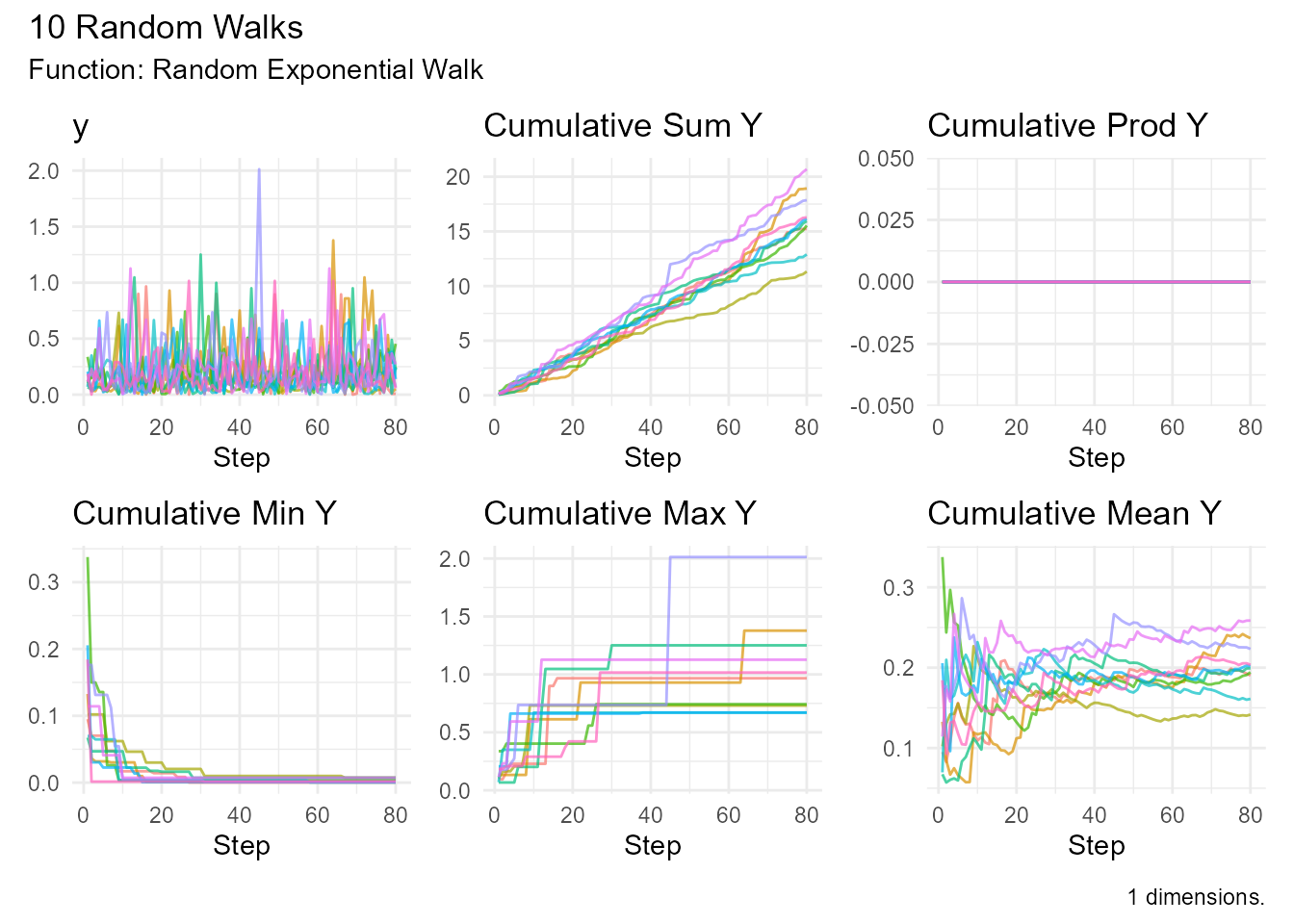

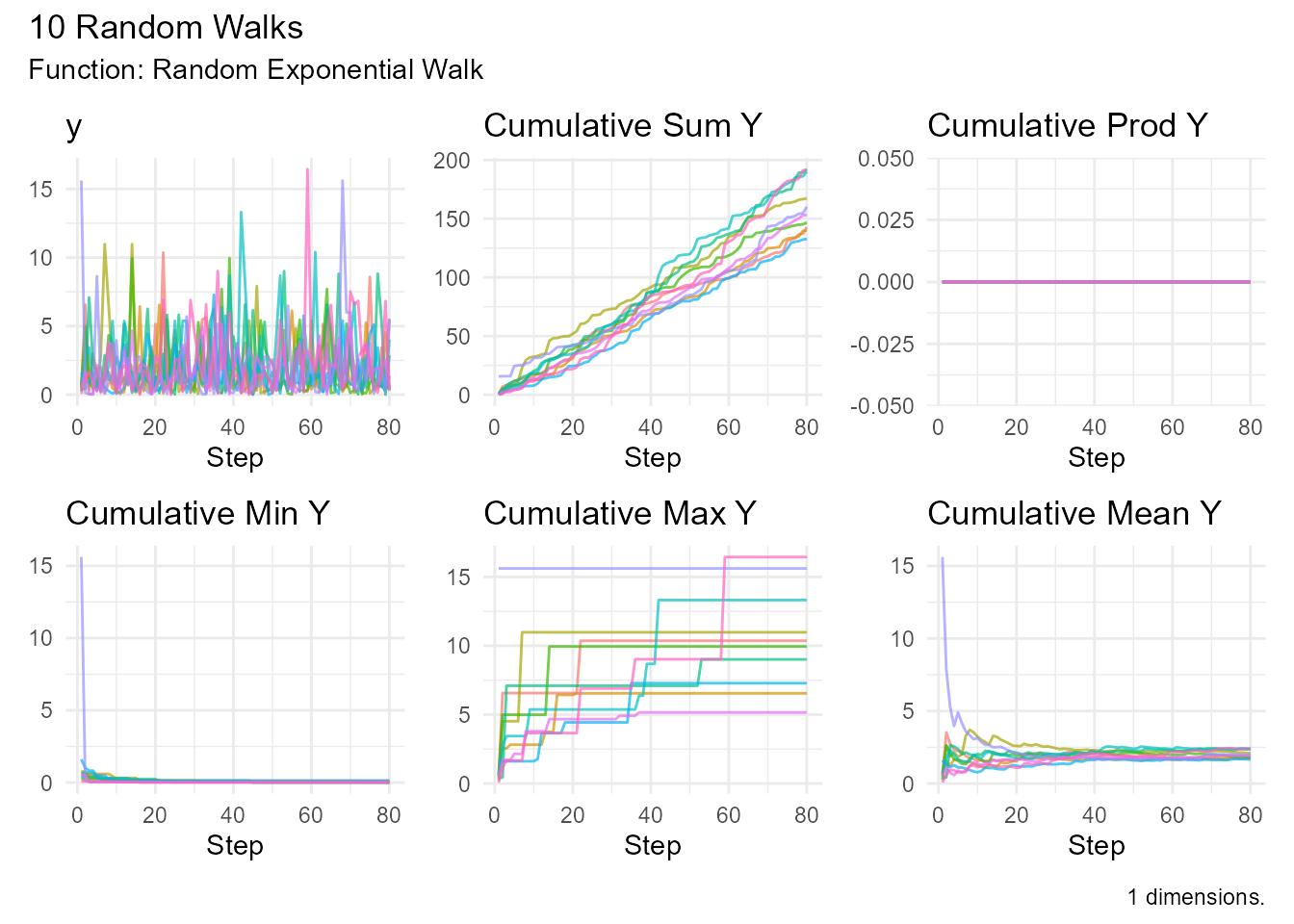

random_exponential_walk()

Random walk with exponentially distributed steps (memoryless property).

Function Signature:

random_exponential_walk(

.num_walks = 25,

.n = 100,

.rate = 1,

.initial_value = 0,

.samp = TRUE,

.replace = TRUE,

.sample_size = 0.8,

.dimensions = 1

)Parameters: - .rate - Rate parameter

(λ)

Properties: - Steps are always positive - Memoryless property - Mean = 1/rate - Variance = 1/rate²

Use Cases: - Time between events (queuing theory) - Lifetime modeling - Radioactive decay - Poisson process intervals

Example:

# Standard exponential

random_exponential_walk(.num_walks = 10) |>

visualize_walks()

# Fast rate (smaller steps)

random_exponential_walk(.num_walks = 10, .rate = 5) |>

visualize_walks()

# Slow rate (larger steps)

random_exponential_walk(.num_walks = 10, .rate = 0.5) |>

visualize_walks()

F Distribution

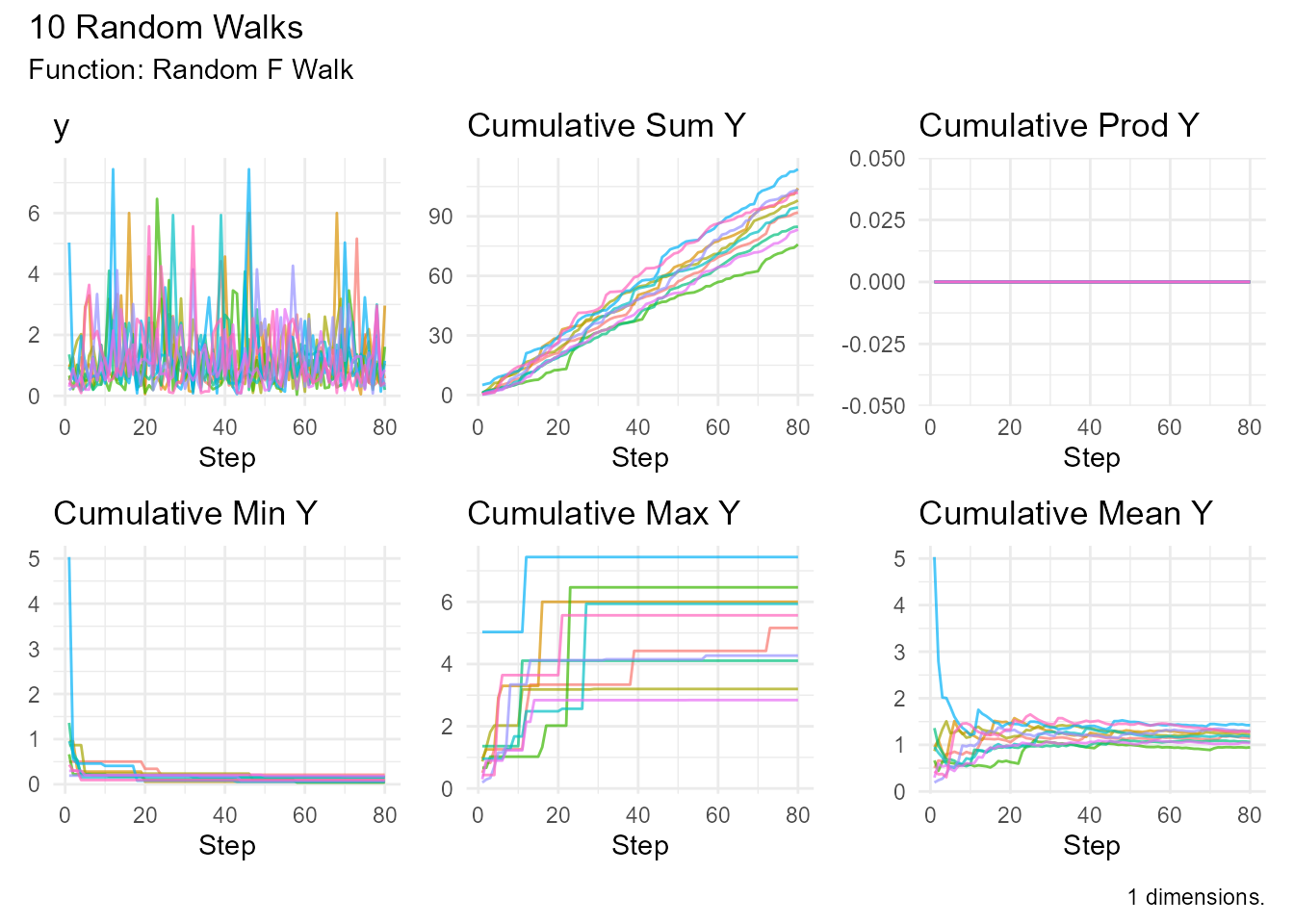

random_f_walk()

Random walk based on F-distribution (ratio of chi-squared variables).

Function Signature:

random_f_walk(

.num_walks = 25,

.n = 100,

.df1 = 5,

.df2 = 5,

.ncp = NULL,

.initial_value = 0,

.samp = TRUE,

.replace = TRUE,

.sample_size = 0.8,

.dimensions = 1

)Parameters: - .df1 - Numerator degrees

of freedom - .df2 - Denominator degrees of freedom -

.ncp - Non-centrality parameter

Use Cases: - ANOVA - Variance ratio tests - Model comparison

Example:

random_f_walk(.num_walks = 10, .df1 = 5, .df2 = 10) |>

visualize_walks()

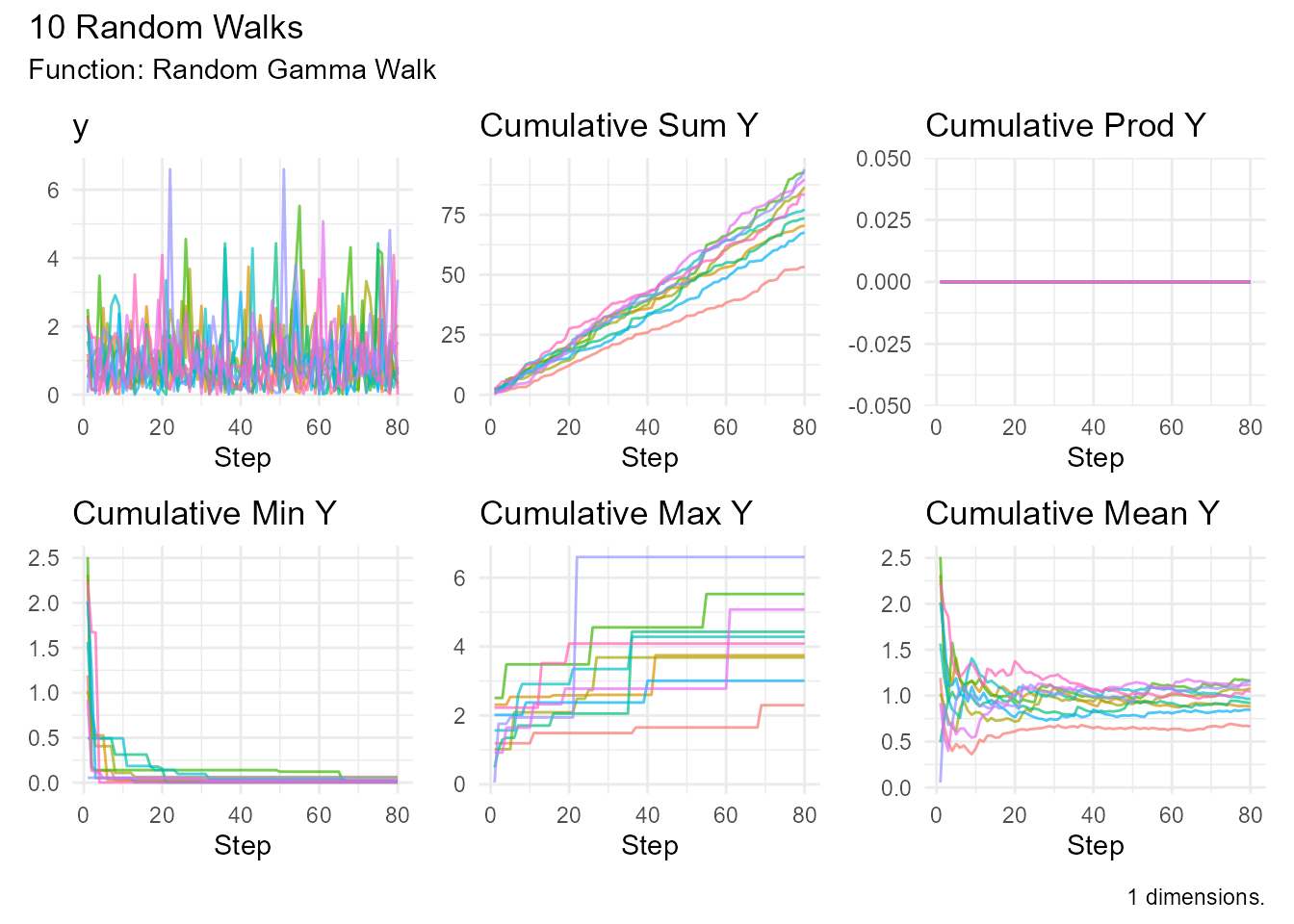

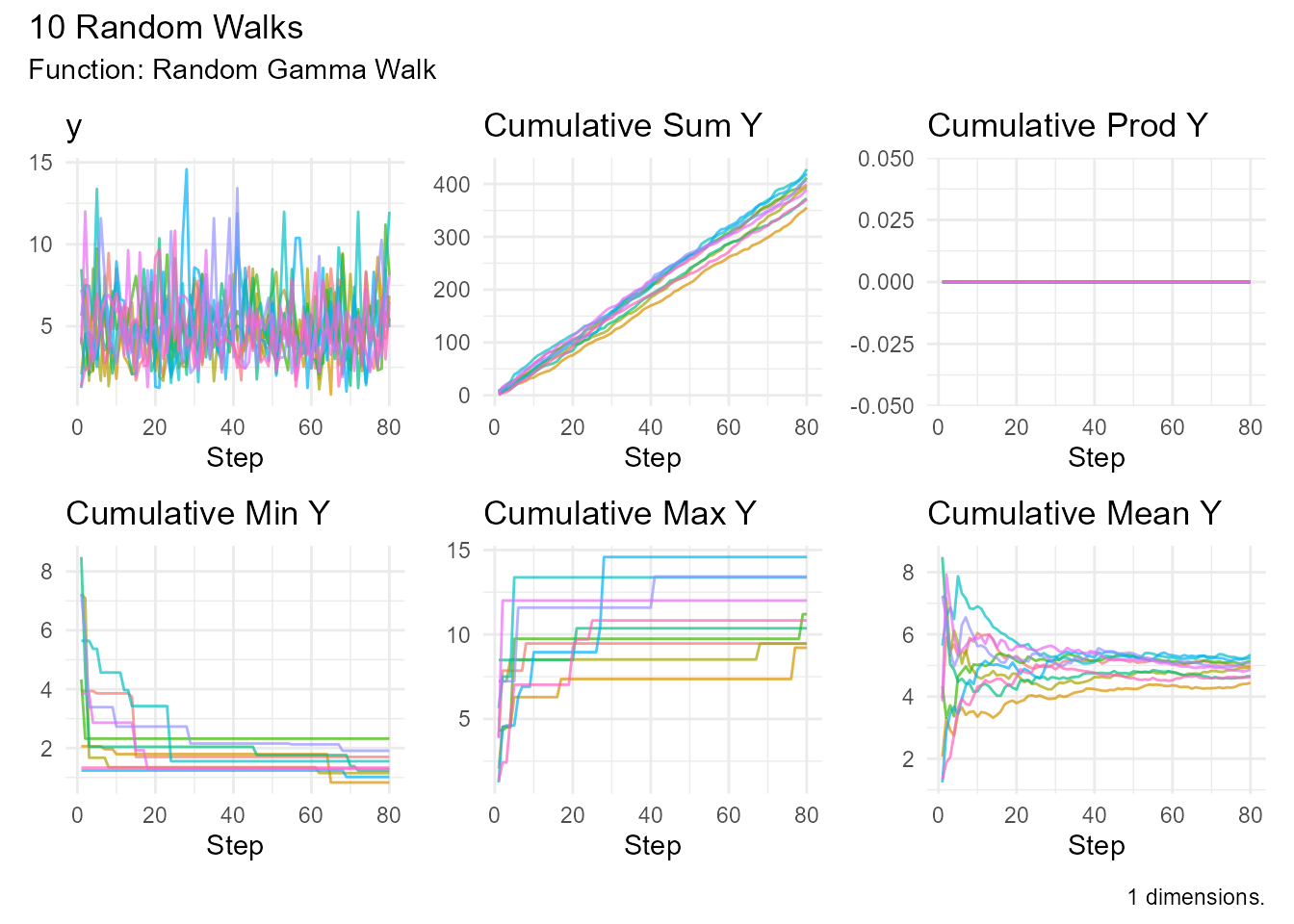

Gamma Distribution

random_gamma_walk()

Flexible distribution for positive values.

Function Signature:

random_gamma_walk(

.num_walks = 25,

.n = 100,

.shape = 1,

.scale = 1,

.rate = NULL,

.initial_value = 0,

.samp = TRUE,

.replace = TRUE,

.sample_size = 0.8,

.dimensions = 1

)Parameters: - .shape - Shape parameter

(k) - .rate - Rate parameter (β) - .scale -

Scale parameter (1/rate)

Properties: - Steps always positive - Flexible shapes - Mean = shape/rate - Variance = shape/rate²

Use Cases: - Waiting times - Rainfall modeling - Insurance claims - Reliability analysis

Example:

# Different shape parameters

random_gamma_walk(.num_walks = 10, .shape = 1, .rate = 1) |>

visualize_walks()

random_gamma_walk(.num_walks = 10, .shape = 5, .rate = 1) |>

visualize_walks()

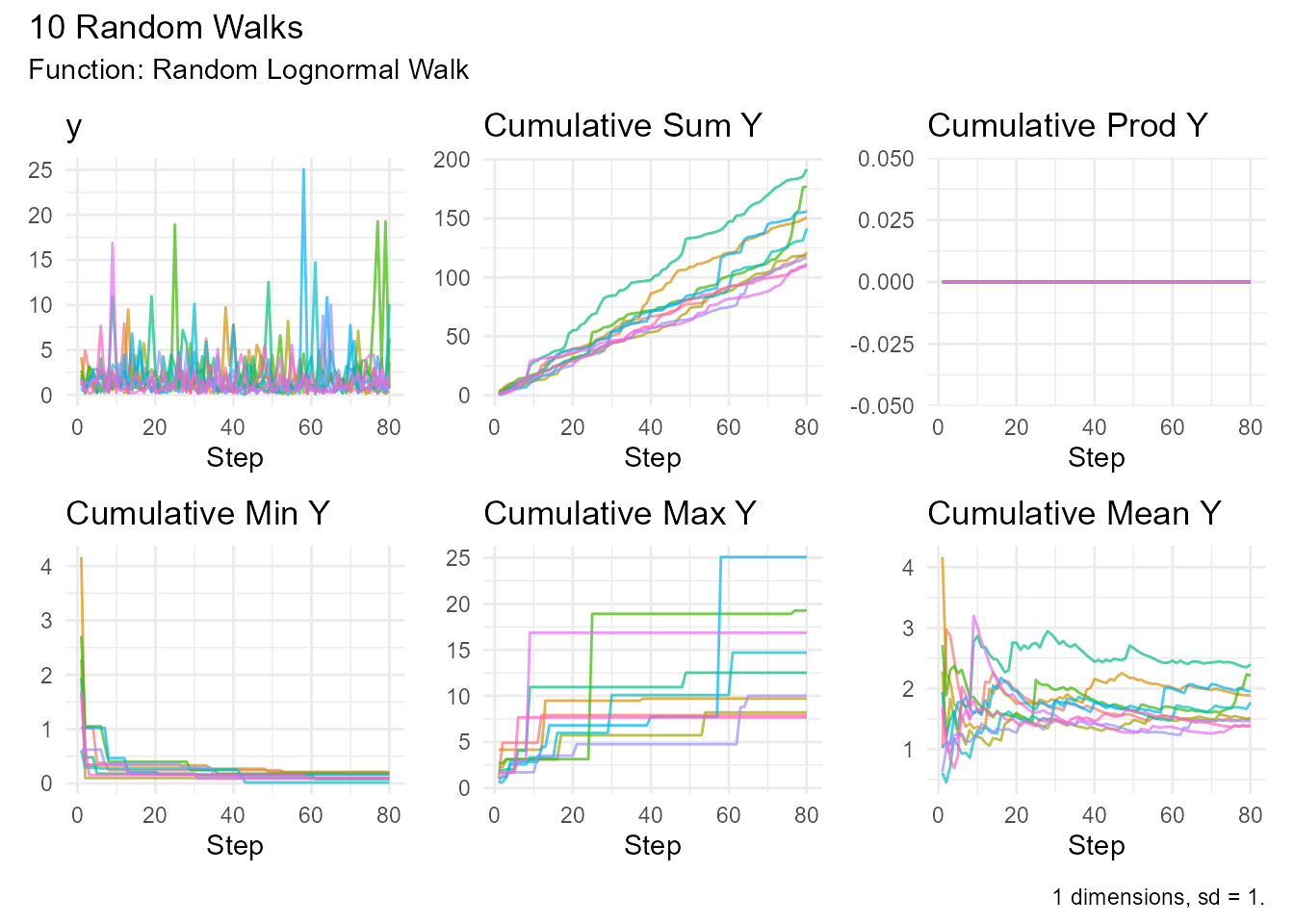

Log-Normal Distribution

random_lognormal_walk()

Random walk where log of steps is normally distributed.

Function Signature:

random_lognormal_walk(

.num_walks = 25,

.n = 100,

.meanlog = 0,

.sdlog = 1,

.initial_value = 0,

.samp = TRUE,

.replace = TRUE,

.sample_size = 0.8,

.dimensions = 1

)Parameters: - .meanlog - Mean of log -

.sdlog - Standard deviation of log

Properties: - Steps always positive - Right-skewed - Multiplicative processes

Use Cases: - Income distributions - File sizes - Particle sizes - Stock prices (alternative to GBM)

Example:

random_lognormal_walk(.num_walks = 10) |>

visualize_walks()

Logistic Distribution

random_logistic_walk()

Random walk with logistic distribution (heavier tails than normal).

Function Signature:

random_logistic_walk(

.num_walks = 25,

.n = 100,

.location = 0,

.scale = 1,

.initial_value = 0,

.samp = TRUE,

.replace = TRUE,

.sample_size = 0.8,

.dimensions = 1

)Use Cases: - Growth models - Binary classification - Neural networks

Example:

random_logistic_walk(.num_walks = 10) |>

visualize_walks()

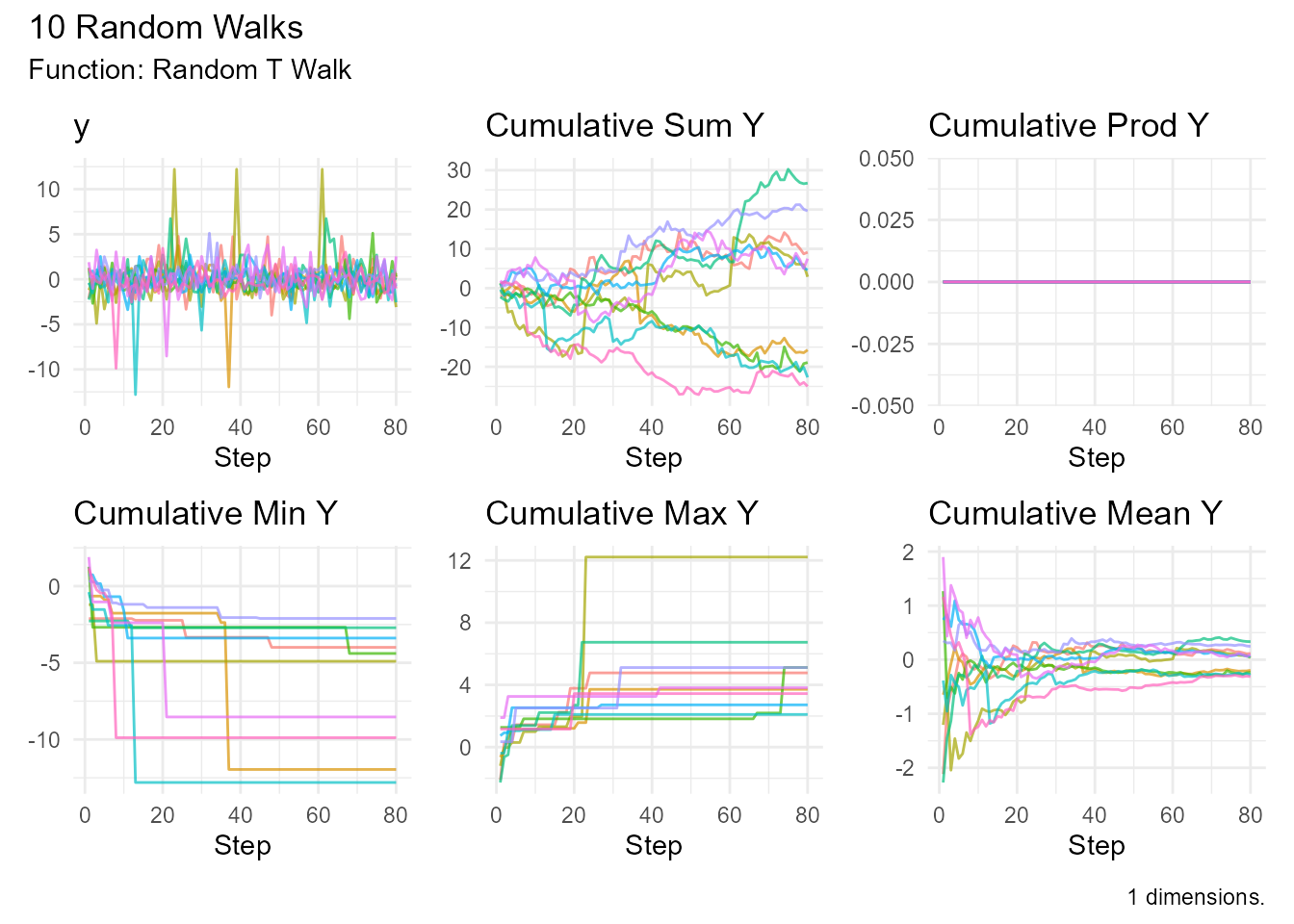

Student’s t Distribution

random_t_walk()

Random walk with t-distribution (adjustable tail heaviness).

Function Signature:

random_t_walk(

.num_walks = 25,

.n = 100,

.df = 5,

.initial_value = 0,

.ncp = 0,

.samp = TRUE,

.replace = TRUE,

.sample_size = 0.8,

.dimensions = 1

)Parameters: - .df - Degrees of freedom

(controls tail heaviness) - .ncp - Non-centrality

parameter

Properties: - Heavier tails than normal (for low df) - Approaches normal as df → ∞ - Mean = 0 (if df > 1) - Variance = df/(df-2) (if df > 2)

Use Cases: - Robust statistics - Small sample inference - Financial returns modeling

Example:

# Heavy tails (df = 3)

random_t_walk(.num_walks = 10, .df = 3) |>

visualize_walks()

# Nearly normal (df = 30)

random_t_walk(.num_walks = 10, .df = 30) |>

visualize_walks()

Uniform Distribution

random_uniform_walk()

Random walk with uniformly distributed steps.

Function Signature:

random_uniform_walk(

.num_walks = 25,

.n = 100,

.min = 0,

.max = 1,

.initial_value = 0,

.samp = TRUE,

.replace = TRUE,

.sample_size = 0.8,

.dimensions = 1

)Parameters: - .min - Minimum value -

.max - Maximum value

Properties: - All values equally likely - Mean = (min + max) / 2 - Variance = (max - min)² / 12

Use Cases: - Modeling equal probabilities - Random sampling - Monte Carlo simulations

Example:

# Symmetric around 0

random_uniform_walk(.num_walks = 10, .min = -1, .max = 1) |>

visualize_walks()

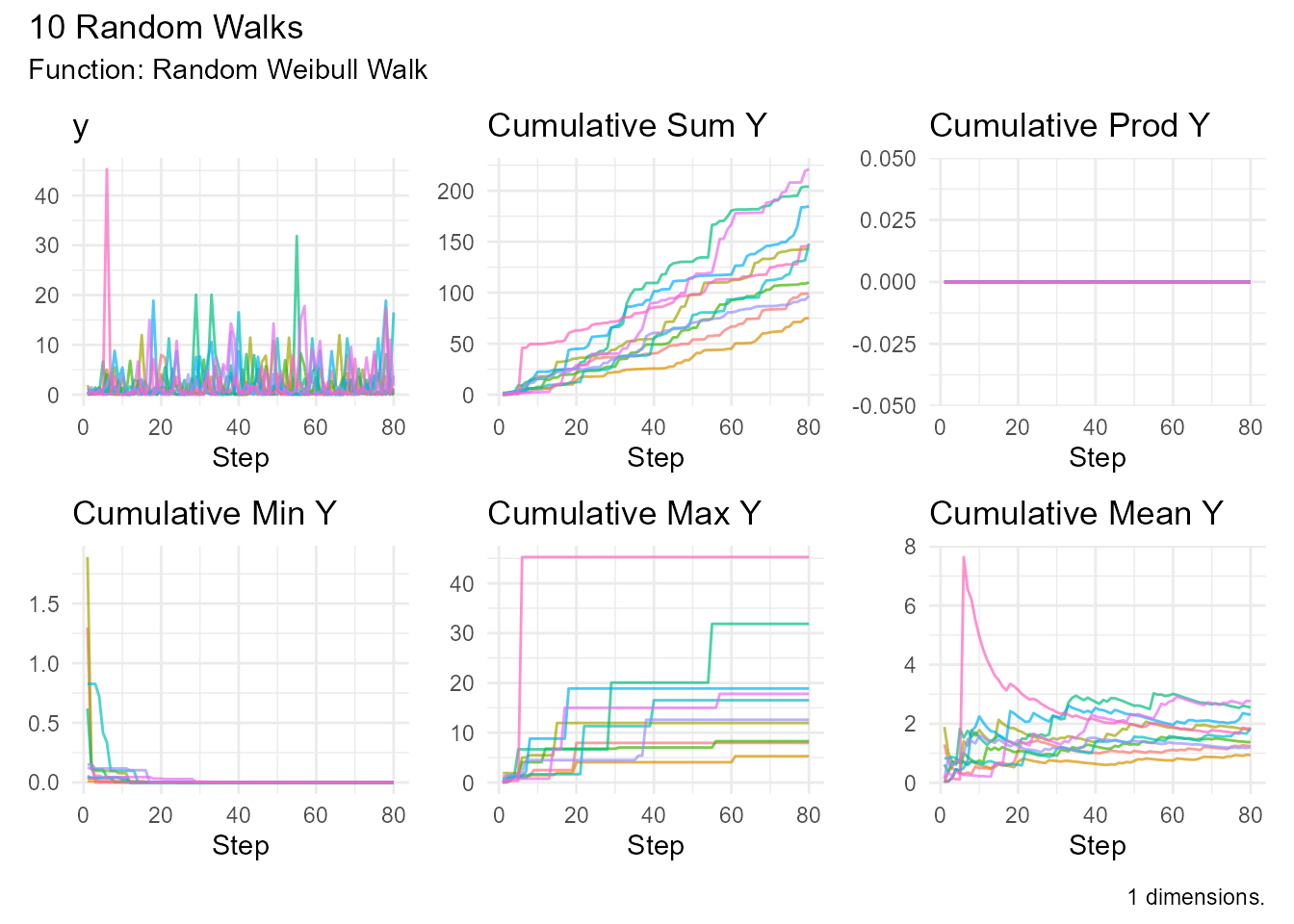

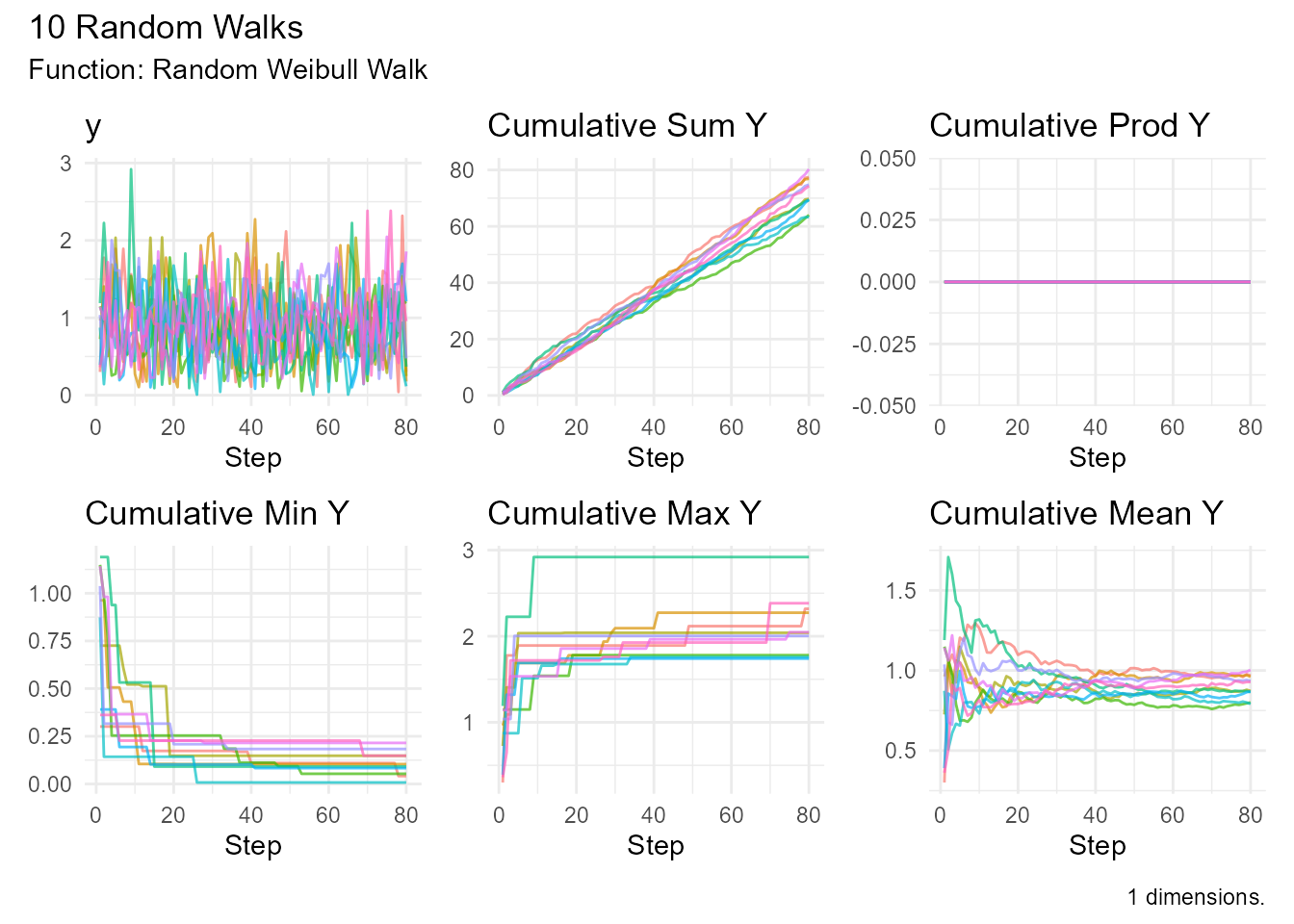

Weibull Distribution

random_weibull_walk()

Random walk with Weibull distribution (flexible lifetime model).

Function Signature:

random_weibull_walk(

.num_walks = 25,

.n = 100,

.shape = 1,

.scale = 1,

.initial_value = 0,

.samp = TRUE,

.replace = TRUE,

.sample_size = 0.8,

.dimensions = 1

)Parameters: - .shape - Shape parameter

(k) - .scale - Scale parameter (λ)

Properties: - Steps always positive - shape < 1: Decreasing failure rate - shape = 1: Constant failure rate (exponential) - shape > 1: Increasing failure rate

Use Cases: - Reliability engineering - Survival analysis - Wind speed modeling - Materials science

Example:

# Different shape parameters

random_weibull_walk(.num_walks = 10, .shape = 0.5) |>

visualize_walks()

random_weibull_walk(.num_walks = 10, .shape = 2) |>

visualize_walks()

Comparison Guide

When to Use Each Distribution

| Distribution | Use When… | Key Property |

|---|---|---|

| Normal | General modeling, natural phenomena | Symmetric, bell-shaped |

| Brownian Motion | Continuous stochastic processes | Foundation of stochastic calculus |

| Geometric Brownian | Stock prices, always positive | Log-normal, multiplicative |

| Beta | Bounded processes (0-1) | Flexible shapes, bounded |

| Cauchy | Extreme events, heavy tails | No mean/variance |

| Chi-Squared | Sum of squares, variance tests | Right-skewed, positive |

| Exponential | Time between events | Memoryless property |

| F | Variance ratios | Ratio of chi-squared |

| Gamma | Positive values, waiting times | Flexible, positive |

| Log-Normal | Multiplicative processes | Right-skewed, positive |

| Logistic | S-curves, classification | Heavier tails than normal |

| Student’s t | Robust modeling, small samples | Adjustable tail heaviness |

| Uniform | Equal probabilities | All values equally likely |

| Weibull | Reliability, survival | Flexible failure rates |