Statistical Analysis Guide

Source:vignettes/statistical-analysis-guide.Rmd

statistical-analysis-guide.RmdRandomWalker provides comprehensive statistical analysis capabilities for random walks. This guide covers all the tools available for analyzing and understanding your random walk data.

Summary Statistics

Basic Summary with summarize_walks()

The summarize_walks() function computes comprehensive

statistics:

# Generate walks

walks <- random_normal_walk(.num_walks = 30, .n = 100)

# Overall summary

walks |> summarize_walks(.value = y)

#> Registered S3 method overwritten by 'quantmod':

#> method from

#> as.zoo.data.frame zoo

#> Warning: There was 1 warning in `dplyr::summarize()`.

#> ℹ In argument: `geometric_mean = exp(mean(log(y)))`.

#> Caused by warning in `log()`:

#> ! NaNs produced

#> # A tibble: 1 × 16

#> fns fns_name obs mean_val median range quantile_lo quantile_hi variance

#> <chr> <chr> <int> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 random… Random … 100 0.00157 0.00383 0.600 -0.190 0.190 0.00935

#> # ℹ 7 more variables: sd <dbl>, min_val <dbl>, max_val <dbl>,

#> # harmonic_mean <dbl>, geometric_mean <dbl>, skewness <dbl>, kurtosis <dbl>

# Summary by walk

walks |>

summarize_walks(.value = y, .group_var = walk_number) |>

head()

#> Warning: There were 30 warnings in `dplyr::summarize()`.

#> The first warning was:

#> ℹ In argument: `geometric_mean = exp(mean(log(y)))`.

#> ℹ In group 1: `walk_number = 1`.

#> Caused by warning in `log()`:

#> ! NaNs produced

#> ℹ Run `dplyr::last_dplyr_warnings()` to see the 29 remaining warnings.

#> # A tibble: 6 × 17

#> walk_number fns fns_name obs mean_val median range quantile_lo

#> <fct> <chr> <chr> <int> <dbl> <dbl> <dbl> <dbl>

#> 1 1 random_normal_w… Random … 100 0.00310 0.0225 0.529 -0.244

#> 2 2 random_normal_w… Random … 100 0.0124 0.00751 0.455 -0.190

#> 3 3 random_normal_w… Random … 100 0.0218 0.0319 0.317 -0.117

#> 4 4 random_normal_w… Random … 100 0.0156 0.0344 0.512 -0.202

#> 5 5 random_normal_w… Random … 100 -0.00789 0.0165 0.374 -0.207

#> 6 6 random_normal_w… Random … 100 0.00755 0.0129 0.479 -0.192

#> # ℹ 9 more variables: quantile_hi <dbl>, variance <dbl>, sd <dbl>,

#> # min_val <dbl>, max_val <dbl>, harmonic_mean <dbl>, geometric_mean <dbl>,

#> # skewness <dbl>, kurtosis <dbl>Statistics Included: - fns - Function

name used to generate walks - fns_name - Formatted function

name - dimensions - Number of dimensions (1, 2, or 3) -

mean_val - Mean of all values - median -

Median value - range - Difference between max and min -

quantile_lo - Lower quantile (default 0.025) -

quantile_hi - Upper quantile (default 0.975) -

variance - Variance - sd - Standard deviation

- min_val - Minimum value - max_val - Maximum

value - harmonic_mean - Harmonic mean -

geometric_mean - Geometric mean - skewness -

Skewness (measure of asymmetry) - kurtosis - Kurtosis

(measure of tail heaviness)

Analyzing Different Values

# Summarize cumulative sum

walks |> summarize_walks(.value = cum_sum_y)

#> Warning: There was 1 warning in `dplyr::summarize()`.

#> ℹ In argument: `geometric_mean = exp(mean(log(cum_sum_y)))`.

#> Caused by warning in `log()`:

#> ! NaNs produced

#> # A tibble: 1 × 16

#> fns fns_name obs mean_val median range quantile_lo quantile_hi variance

#> <chr> <chr> <int> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 random_… Random … 100 0.0715 0.0761 4.98 -1.24 1.45 0.456

#> # ℹ 7 more variables: sd <dbl>, min_val <dbl>, max_val <dbl>,

#> # harmonic_mean <dbl>, geometric_mean <dbl>, skewness <dbl>, kurtosis <dbl>

# Summarize cumulative product

geometric_brownian_motion(.num_walks = 30, .initial_value = 100) |>

summarize_walks(.value = cum_prod_y)

#> # A tibble: 1 × 17

#> fns fns_name dimensions obs mean_val median range quantile_lo

#> <chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 geometric_brow… Geometr… 1 100 7.72e30 1.66e17 2.89e33 800.

#> # ℹ 9 more variables: quantile_hi <dbl>, variance <dbl>, sd <dbl>,

#> # min_val <dbl>, max_val <dbl>, harmonic_mean <dbl>, geometric_mean <dbl>,

#> # skewness <dbl>, kurtosis <dbl>

# Summarize by group

walks |>

summarize_walks(.value = cum_sum_y, .group_var = walk_number) |>

head()

#> Warning: There were 29 warnings in `dplyr::summarize()`.

#> The first warning was:

#> ℹ In argument: `geometric_mean = exp(mean(log(cum_sum_y)))`.

#> ℹ In group 1: `walk_number = 1`.

#> Caused by warning in `log()`:

#> ! NaNs produced

#> ℹ Run `dplyr::last_dplyr_warnings()` to see the 28 remaining warnings.

#> # A tibble: 6 × 17

#> walk_number fns fns_name obs mean_val median range quantile_lo

#> <fct> <chr> <chr> <int> <dbl> <dbl> <dbl> <dbl>

#> 1 1 random_normal_w… Random … 100 -0.0272 -0.0154 0.998 -0.529

#> 2 2 random_normal_w… Random … 100 0.283 0.212 1.41 -0.267

#> 3 3 random_normal_w… Random … 100 1.00 1.32 1.77 0.00822

#> 4 4 random_normal_w… Random … 100 1.13 1.24 1.58 0.102

#> 5 5 random_normal_w… Random … 100 -0.544 -0.513 1.05 -0.944

#> 6 6 random_normal_w… Random … 100 0.197 0.284 0.957 -0.287

#> # ℹ 9 more variables: quantile_hi <dbl>, variance <dbl>, sd <dbl>,

#> # min_val <dbl>, max_val <dbl>, harmonic_mean <dbl>, geometric_mean <dbl>,

#> # skewness <dbl>, kurtosis <dbl>Understanding Output Columns

Location Measures: - mean_val: Average

value across all observations - median: Middle value (50th

percentile) - harmonic_mean: Harmonic mean (useful for

rates and ratios) - geometric_mean: Geometric mean (useful

for growth rates)

Dispersion Measures: - variance:

Average squared deviation from mean - sd: Standard

deviation (square root of variance) - range: Max - Min -

quantile_lo / quantile_hi: Lower and upper

quantiles

Shape Measures: - skewness: - = 0:

Symmetric distribution - > 0: Right-skewed (tail extends right) -

< 0: Left-skewed (tail extends left) - kurtosis: - ≈ 3:

Normal distribution - > 3: Heavy tails (more extreme values) - <

3: Light tails (fewer extreme values)

Practical Examples

Example 1: Analyzing Stock Price Simulations

# Simulate stock prices

stock_sim <- geometric_brownian_motion(

.num_walks = 1000,

.n = 252, # Trading days

.mu = 0.08,

.sigma = 0.25,

.initial_value = 100

)

# Get final price statistics

final_prices <- stock_sim |>

summarize_walks(.value = cum_prod_y, .group_var = walk_number) |>

pull(max_val)

# Analyze outcomes

tibble(final_price = final_prices) |>

summarize(

median_price = median(final_price),

mean_price = mean(final_price),

prob_profit = mean(final_price > 100),

prob_loss_20 = mean(final_price < 80),

sd_returns = sd((final_price - 100) / 100)

)

#> # A tibble: 1 × 5

#> median_price mean_price prob_profit prob_loss_20 sd_returns

#> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 1.17e79 1.45e102 1 0 4.50e101Example 2: Comparing Distributions

# Normal vs Cauchy walks

normal_stats <- random_normal_walk(.num_walks = 100, .n = 100) |>

summarize_walks(.value = y) |>

mutate(distribution = "Normal")

#> Warning: There was 1 warning in `dplyr::summarize()`.

#> ℹ In argument: `geometric_mean = exp(mean(log(y)))`.

#> Caused by warning in `log()`:

#> ! NaNs produced

cauchy_stats <- random_cauchy_walk(.num_walks = 100, .n = 100) |>

summarize_walks(.value = y) |>

mutate(distribution = "Cauchy")

#> Warning: There was 1 warning in `dplyr::summarize()`.

#> ℹ In argument: `geometric_mean = exp(mean(log(y)))`.

#> Caused by warning in `log()`:

#> ! NaNs produced

# Compare

bind_rows(normal_stats, cauchy_stats) |>

select(distribution, mean_val, sd, skewness, kurtosis)

#> # A tibble: 2 × 5

#> distribution mean_val sd skewness kurtosis

#> <chr> <dbl> <dbl> <dbl> <dbl>

#> 1 Normal -0.000687 0.0989 -0.0550 -0.0309

#> 2 Cauchy 0.266 90.1 -1.79 2730.Cumulative Functions

RandomWalker automatically computes several cumulative functions for each walk.

Available Cumulative Functions

For 1D Walks: - cum_sum - Cumulative

sum: ∑ y - cum_prod - Cumulative product: ∏ (1 + y) -

cum_min - Cumulative minimum: min(y₁, y₂, …, yₙ) -

cum_max - Cumulative maximum: max(y₁, y₂, …, yₙ) -

cum_mean - Cumulative mean: (∑ y) / n

For Multi-Dimensional Walks: Cumulative functions are computed for each dimension (x, y, z).

Using Cumulative Functions

# Generate walk

walks <- random_normal_walk(.num_walks = 10, .n = 100, .initial_value = 100)

# Cumulative functions are already in the data

walks |>

select(walk_number, step_number, y, starts_with("cum_")) |>

head(10)

#> # A tibble: 10 × 8

#> walk_number step_number y cum_sum_y cum_prod_y cum_min_y cum_max_y

#> <fct> <int> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 1 1 0.0840 100. 108. 100. 100.

#> 2 1 2 0.0469 100. 113. 100. 100.

#> 3 1 3 0.00691 100. 114. 100. 100.

#> 4 1 4 -0.136 100. 98.8 99.9 100.

#> 5 1 5 0.00489 100. 99.3 99.9 100.

#> 6 1 6 -0.0991 99.9 89.4 99.9 100.

#> 7 1 7 -0.0305 99.9 86.7 99.9 100.

#> 8 1 8 0.0961 100.0 95.0 99.9 100.

#> 9 1 9 0.0238 100.0 97.3 99.9 100.

#> 10 1 10 -0.00424 100.0 96.9 99.9 100.

#> # ℹ 1 more variable: cum_mean_y <dbl>

# Analyze cumulative sum

walks |>

summarize_walks(.value = cum_sum_y, .group_var = walk_number) |>

head()

#> # A tibble: 6 × 17

#> walk_number fns fns_name obs mean_val median range quantile_lo quantile_hi

#> <fct> <chr> <chr> <int> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 1 rand… Random … 100 101. 101. 1.50 100.0 101.

#> 2 2 rand… Random … 100 100. 100. 0.916 99.6 100.

#> 3 3 rand… Random … 100 98.9 98.9 1.82 98.3 100.0

#> 4 4 rand… Random … 100 100. 100. 0.861 99.7 100.

#> 5 5 rand… Random … 100 100. 100. 1.15 100. 101.

#> 6 6 rand… Random … 100 99.8 99.8 0.894 99.4 100.

#> # ℹ 8 more variables: variance <dbl>, sd <dbl>, min_val <dbl>, max_val <dbl>,

#> # harmonic_mean <dbl>, geometric_mean <dbl>, skewness <dbl>, kurtosis <dbl>

# Track maximum ever reached

walks |>

group_by(walk_number) |>

summarize(

max_ever = max(cum_max_y),

min_ever = min(cum_min_y),

final_value = last(cum_sum_y)

) |>

head()

#> # A tibble: 6 × 4

#> walk_number max_ever min_ever final_value

#> <fct> <dbl> <dbl> <dbl>

#> 1 1 100. 99.8 100.

#> 2 2 100. 99.8 100.

#> 3 3 100. 99.8 98.3

#> 4 4 100. 99.8 101.

#> 5 5 100. 99.8 101.

#> 6 6 100. 99.8 100.Custom Cumulative Functions

Add your own cumulative calculations:

# Add custom cumulative functions

walks_extended <- walks |>

group_by(walk_number) |>

mutate(

# Cumulative variance

cum_var = cumsum((y - cumsum(y) / row_number())^2) / row_number(),

# Cumulative absolute sum

cum_abs_sum = cumsum(abs(y)),

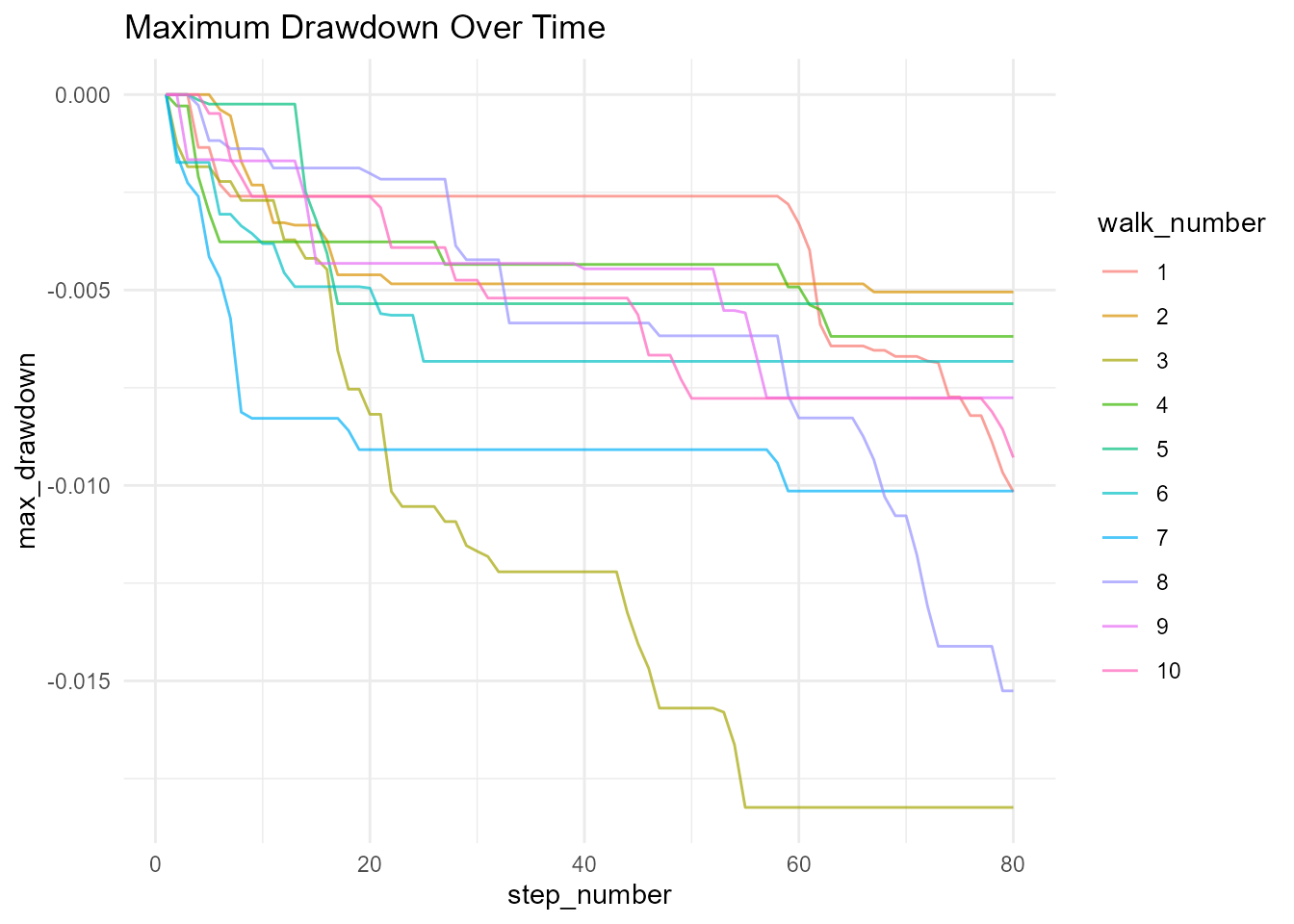

# Running maximum drawdown

running_peak = cummax(cum_sum_y),

drawdown = (cum_sum_y - running_peak) / running_peak,

max_drawdown = cummin(drawdown)

) |>

ungroup()

# Visualize drawdown

walks_extended |>

ggplot(aes(x = step_number, y = max_drawdown, color = walk_number)) +

geom_line(alpha = 0.7) +

theme_minimal() +

labs(title = "Maximum Drawdown Over Time")

Confidence Intervals

Using confidence_interval()

Calculate confidence intervals for a vector:

# Generate data

x <- rnorm(1000, mean = 10, sd = 2)

# Calculate 95% CI (default)

confidence_interval(x)

#> # A tibble: 1 × 2

#> lower upper

#> <dbl> <dbl>

#> 1 9.88 10.1

# Calculate 99% CI

confidence_interval(x, .interval = 0.01)

#> # A tibble: 1 × 2

#> lower upper

#> <dbl> <dbl>

#> 1 10.00 10.0

# Calculate 90% CI

confidence_interval(x, .interval = 0.10)

#> # A tibble: 1 × 2

#> lower upper

#> <dbl> <dbl>

#> 1 9.99 10.0Confidence Intervals for Random Walks

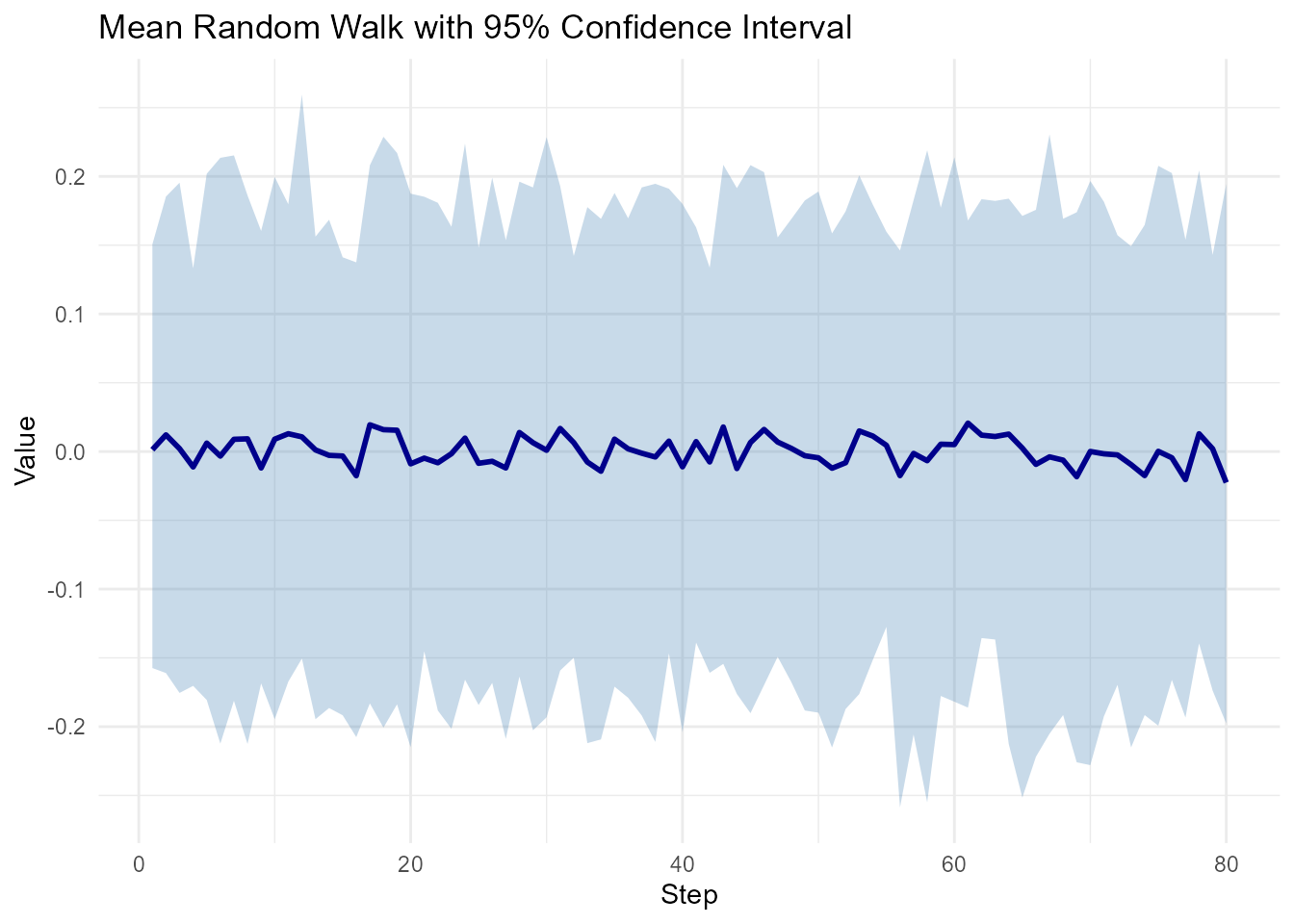

# Generate walks

walks <- random_normal_walk(.num_walks = 100, .n = 100)

# Calculate CI at each step

ci_by_step <- walks |>

group_by(step_number) |>

summarize(

mean_val = mean(y),

lower = quantile(y, 0.025),

upper = quantile(y, 0.975)

)

# Visualize

ggplot(ci_by_step, aes(x = step_number)) +

geom_ribbon(aes(ymin = lower, ymax = upper), alpha = 0.3, fill = "steelblue") +

geom_line(aes(y = mean_val), color = "darkblue", linewidth = 1) +

theme_minimal() +

labs(

title = "Mean Random Walk with 95% Confidence Interval",

x = "Step",

y = "Value"

)

Confidence Intervals for Final Values

# Get final values from many walks

walks <- random_normal_walk(.num_walks = 1000, .n = 100, .initial_value = 100)

final_values <- walks |>

group_by(walk_number) |>

slice_max(step_number, n = 1) |>

pull(cum_sum_y)

# Calculate confidence interval

confidence_interval(final_values)

#> # A tibble: 1 × 2

#> lower upper

#> <dbl> <dbl>

#> 1 100.0 100.Running Quantiles

Using running_quantile()

Calculate quantiles at each position:

# Generate walks

walks <- random_normal_walk(.num_walks = 100, .n = 100)

# Calculate running median (50th percentile)

walks_with_median <- walks |>

group_by(step_number) |>

mutate(median_at_step = running_quantile(y, .probs = 0.5, .window = 5)) |>

ungroup()

# Show results

walks_with_median |>

select(walk_number, step_number, y, median_at_step) |>

head(10)

#> # A tibble: 10 × 4

#> walk_number step_number y median_at_step

#> <fct> <int> <dbl> <dbl>

#> 1 1 1 0.123 0.000678

#> 2 1 2 0.0201 0.0201

#> 3 1 3 -0.0235 -0.0235

#> 4 1 4 -0.0535 -0.0535

#> 5 1 5 -0.00384 -0.00384

#> 6 1 6 -0.122 -0.0440

#> 7 1 7 -0.0933 -0.0440

#> 8 1 8 -0.0562 -0.0562

#> 9 1 9 0.233 -0.0513

#> 10 1 10 -0.0647 -0.0647

# Calculate running quartiles

walks_with_quartiles <- walks |>

group_by(step_number) |>

mutate(

q25 = running_quantile(y, .probs = 0.25, .window = 5),

q50 = running_quantile(y, .probs = 0.50, .window = 5),

q75 = running_quantile(y, .probs = 0.75, .window = 5)

) |>

ungroup()

# Show results

walks_with_quartiles |>

select(walk_number, step_number, y, q25, q50, q75) |>

head(10)

#> # A tibble: 10 × 6

#> walk_number step_number y q25 q50 q75

#> <fct> <int> <dbl> <dbl> <dbl> <dbl>

#> 1 1 1 0.123 -0.0255 0.000678 0.0619

#> 2 1 2 0.0201 0.0151 0.0201 0.0238

#> 3 1 3 -0.0235 -0.0259 -0.0235 0.0187

#> 4 1 4 -0.0535 -0.0548 -0.0535 0.0653

#> 5 1 5 -0.00384 -0.0883 -0.00384 0.0308

#> 6 1 6 -0.122 -0.0831 -0.0440 0.00787

#> 7 1 7 -0.0933 -0.0687 -0.0440 -0.0254

#> 8 1 8 -0.0562 -0.104 -0.0562 0.0533

#> 9 1 9 0.233 -0.0592 -0.0513 0.0906

#> 10 1 10 -0.0647 -0.125 -0.0647 0.0415Visualizing Quantile Evolution

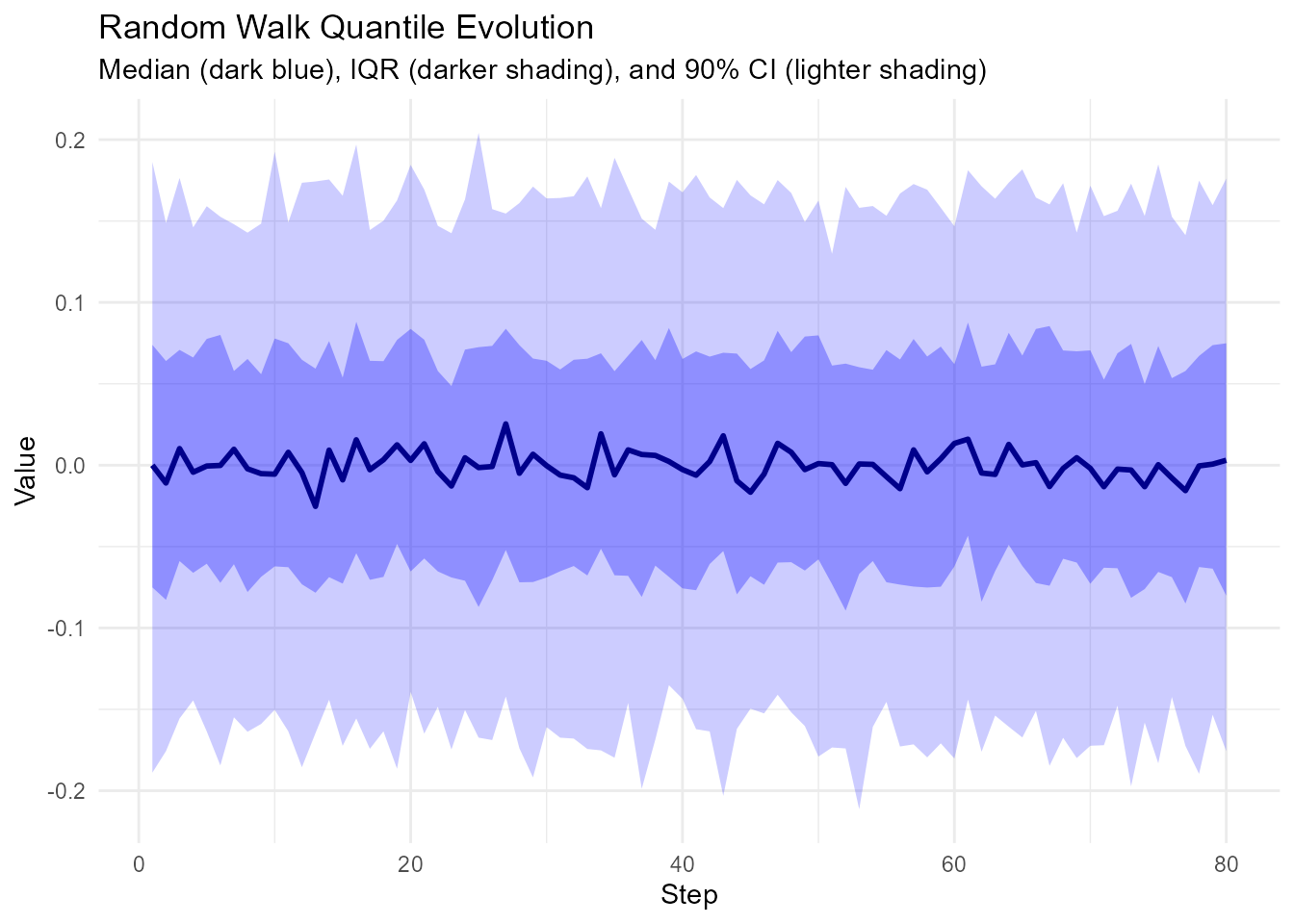

# Generate many walks

walks <- random_normal_walk(.num_walks = 200, .n = 100)

# Calculate quantiles at each step

quantile_evolution <- walks |>

group_by(step_number) |>

summarize(

q05 = quantile(y, 0.05),

q25 = quantile(y, 0.25),

q50 = quantile(y, 0.50),

q75 = quantile(y, 0.75),

q95 = quantile(y, 0.95)

)

# Plot

ggplot(quantile_evolution, aes(x = step_number)) +

geom_ribbon(aes(ymin = q05, ymax = q95), alpha = 0.2, fill = "blue") +

geom_ribbon(aes(ymin = q25, ymax = q75), alpha = 0.3, fill = "blue") +

geom_line(aes(y = q50), color = "darkblue", linewidth = 1) +

theme_minimal() +

labs(

title = "Random Walk Quantile Evolution",

subtitle = "Median (dark blue), IQR (darker shading), and 90% CI (lighter shading)",

x = "Step",

y = "Value"

)

Distance Calculations

Using euclidean_distance()

For multi-dimensional walks, calculate distance from origin:

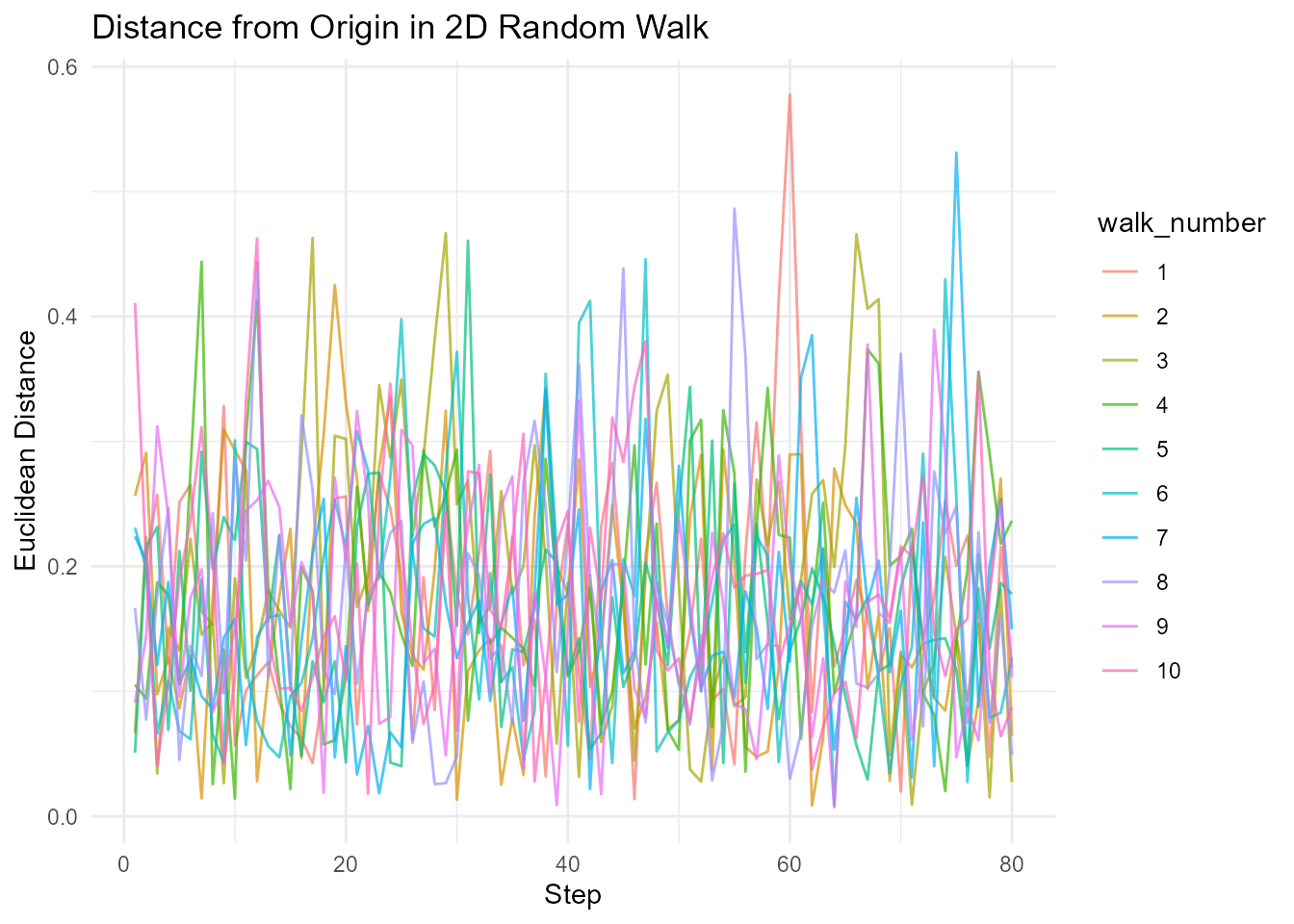

# 2D walk

walks_2d <- random_normal_walk(.num_walks = 10, .n = 100, .dimensions = 2)

# Calculate Euclidean distance

walks_with_distance <- walks_2d |>

euclidean_distance(.x = x, .y = y)

# Visualize distance over time

walks_with_distance |>

ggplot(aes(x = step_number, y = distance, color = walk_number)) +

geom_line(alpha = 0.7) +

theme_minimal() +

labs(

title = "Distance from Origin in 2D Random Walk",

x = "Step",

y = "Euclidean Distance"

)

#> Warning: Removed 1 row containing missing values or values outside the scale range

#> (`geom_line()`).

Distance Statistics

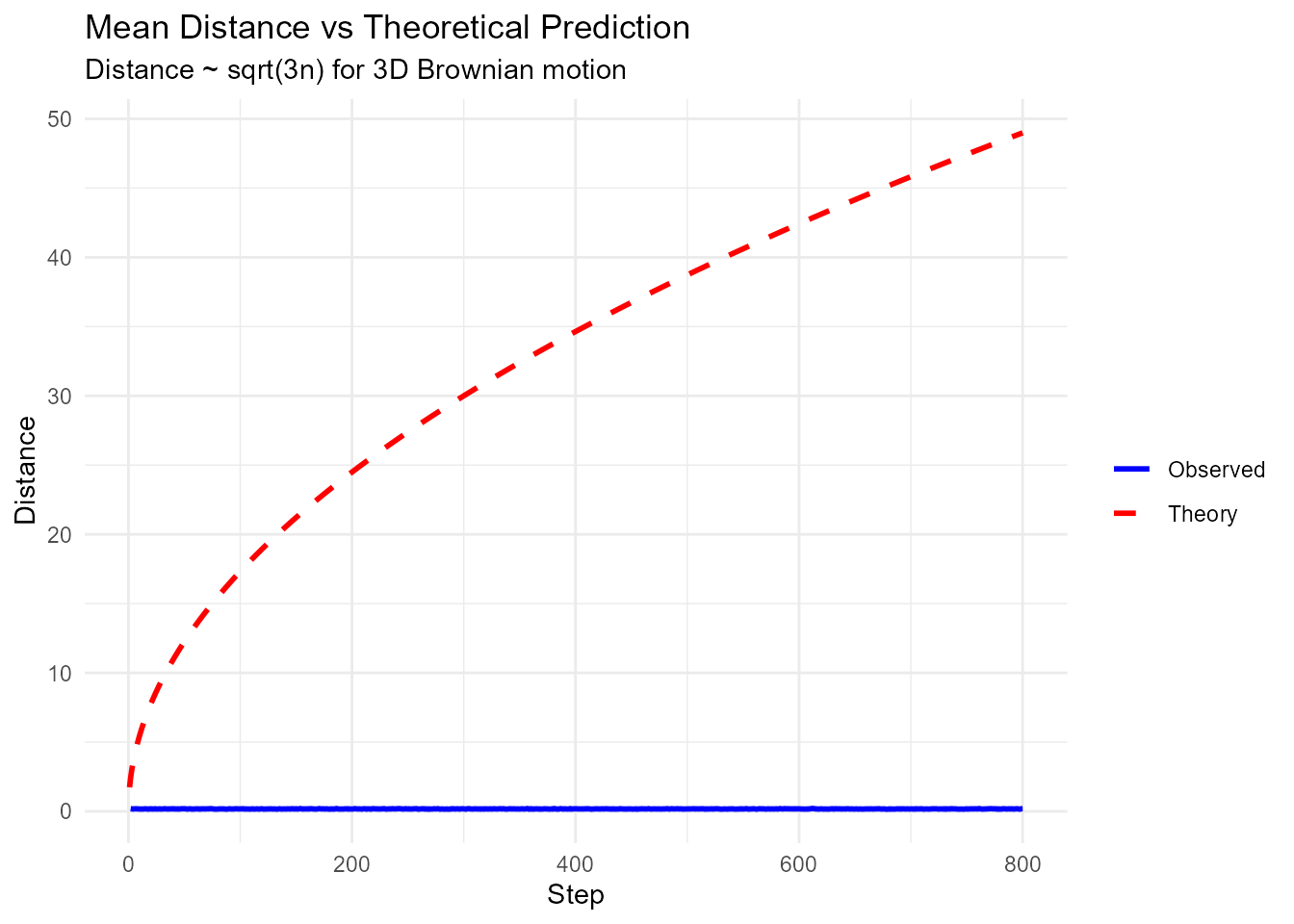

# 3D walk

walks_3d <- random_normal_walk(.num_walks = 100, .n = 1000, .dimensions = 3)

# Calculate distance

walks_with_dist <- walks_3d |> euclidean_distance(.x = x, .y = z)

# Analyze distance evolution

distance_stats <- walks_with_dist |>

group_by(step_number) |>

summarize(

mean_dist = mean(distance),

sd_dist = sd(distance),

max_dist = max(distance)

)

# Plot average distance vs sqrt(n) theoretical prediction

distance_stats |>

ggplot(aes(x = step_number)) +

geom_line(aes(y = mean_dist, color = "Observed"), linewidth = 1) +

geom_line(aes(y = sqrt(3 * step_number), color = "Theory"), linewidth = 1, linetype = "dashed") +

scale_color_manual(values = c("Observed" = "blue", "Theory" = "red")) +

theme_minimal() +

labs(

title = "Mean Distance vs Theoretical Prediction",

subtitle = "Distance ~ sqrt(3n) for 3D Brownian motion",

x = "Step",

y = "Distance",

color = ""

)

#> Warning: Removed 1 row containing missing values or values outside the scale range

#> (`geom_line()`).

First Passage Time

Calculate when walks first reach a threshold:

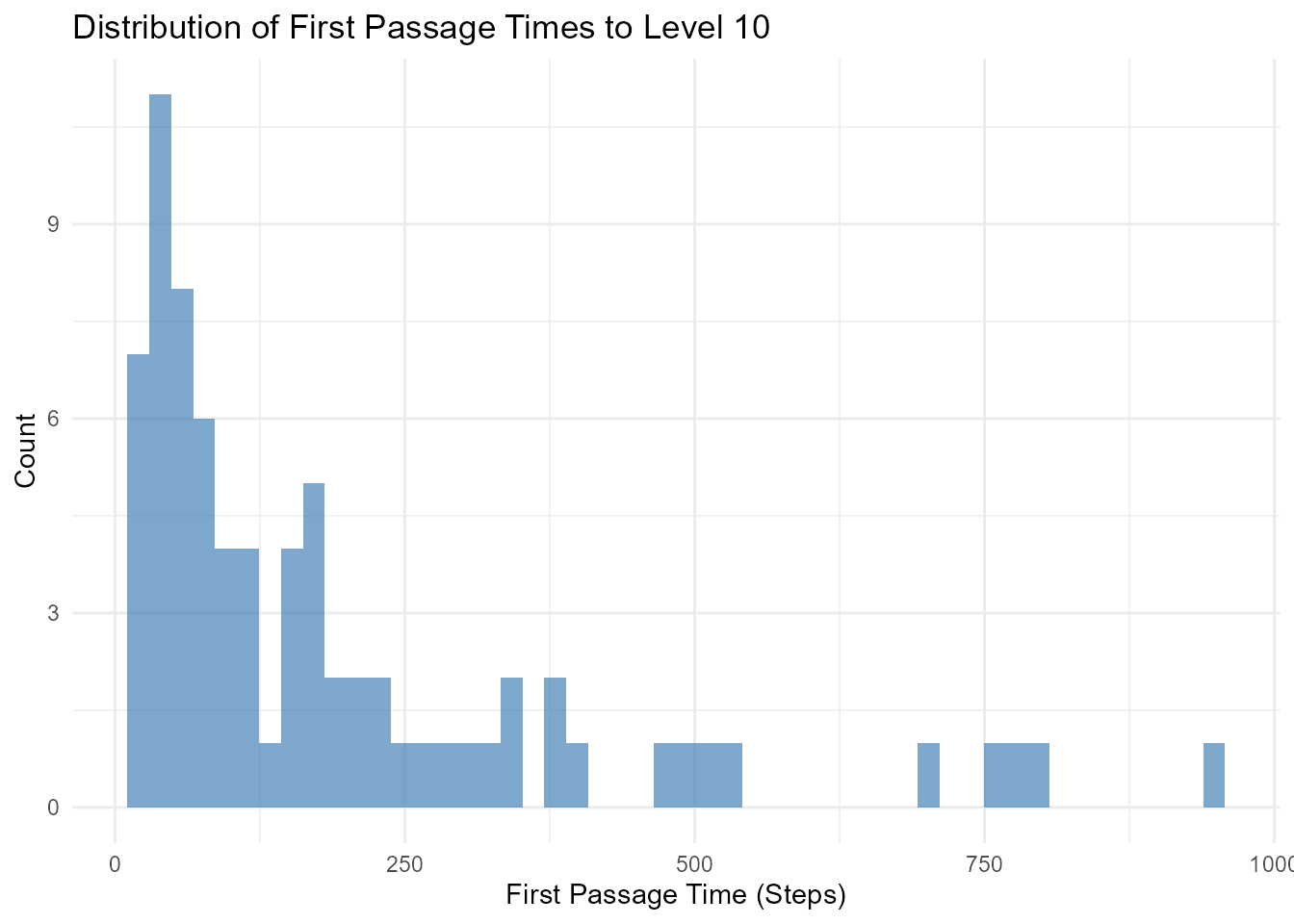

# Generate walks

walks <- discrete_walk(.num_walks = 100, .n = 1000, .initial_value = 0)

# Find first passage time to level 10

first_passage <- walks |>

group_by(walk_number) |>

filter(cum_sum_y >= 10) |>

slice_min(step_number, n = 1) |>

select(walk_number, first_passage_time = step_number)

# Analyze distribution of first passage times

first_passage |>

ggplot(aes(x = first_passage_time)) +

geom_histogram(bins = 50, fill = "steelblue", alpha = 0.7) +

theme_minimal() +

labs(

title = "Distribution of First Passage Times to Level 10",

x = "First Passage Time (Steps)",

y = "Count"

)

Subsetting Walks

Using subset_walks()

Extract walks with extreme values:

# Generate walks

walks <- random_normal_walk(.num_walks = 100, .n = 100, .initial_value = 100)

# Get walk with maximum final value

max_walk <- walks |> subset_walks(.value = "cum_sum_y", .type = "max")

# Get walk with minimum final value

min_walk <- walks |> subset_walks(.value = "cum_sum_y", .type = "min")

# Show the extreme walks

max_walk |>

summarize_walks(.value = cum_sum_y, .group_var = walk_number)

#> # A tibble: 1 × 17

#> walk_number fns fns_name obs mean_val median range quantile_lo quantile_hi

#> <fct> <chr> <chr> <int> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 21 rand… Random … 100 101. 101. 2.86 100. 103.

#> # ℹ 8 more variables: variance <dbl>, sd <dbl>, min_val <dbl>, max_val <dbl>,

#> # harmonic_mean <dbl>, geometric_mean <dbl>, skewness <dbl>, kurtosis <dbl>

min_walk |>

summarize_walks(.value = cum_sum_y, .group_var = walk_number)

#> # A tibble: 1 × 17

#> walk_number fns fns_name obs mean_val median range quantile_lo quantile_hi

#> <fct> <chr> <chr> <int> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 66 rand… Random … 100 98.3 98.3 2.84 97.2 99.8

#> # ℹ 8 more variables: variance <dbl>, sd <dbl>, min_val <dbl>, max_val <dbl>,

#> # harmonic_mean <dbl>, geometric_mean <dbl>, skewness <dbl>, kurtosis <dbl>Finding Specific Walks

# Find walks that cross a threshold

walks <- random_normal_walk(.num_walks = 100, .n = 100, .initial_value = 100)

# Identify walks that reached 102

crossed_102 <- walks |>

group_by(walk_number) |>

filter(any(cum_sum_y >= 102)) |>

pull(walk_number) |>

unique()

# Extract and visualize those walks

walks |>

filter(walk_number %in% crossed_102) |>

visualize_walks(.pluck = "cum_sum", .alpha = 0.3)

Advanced Analysis

Autocorrelation Analysis

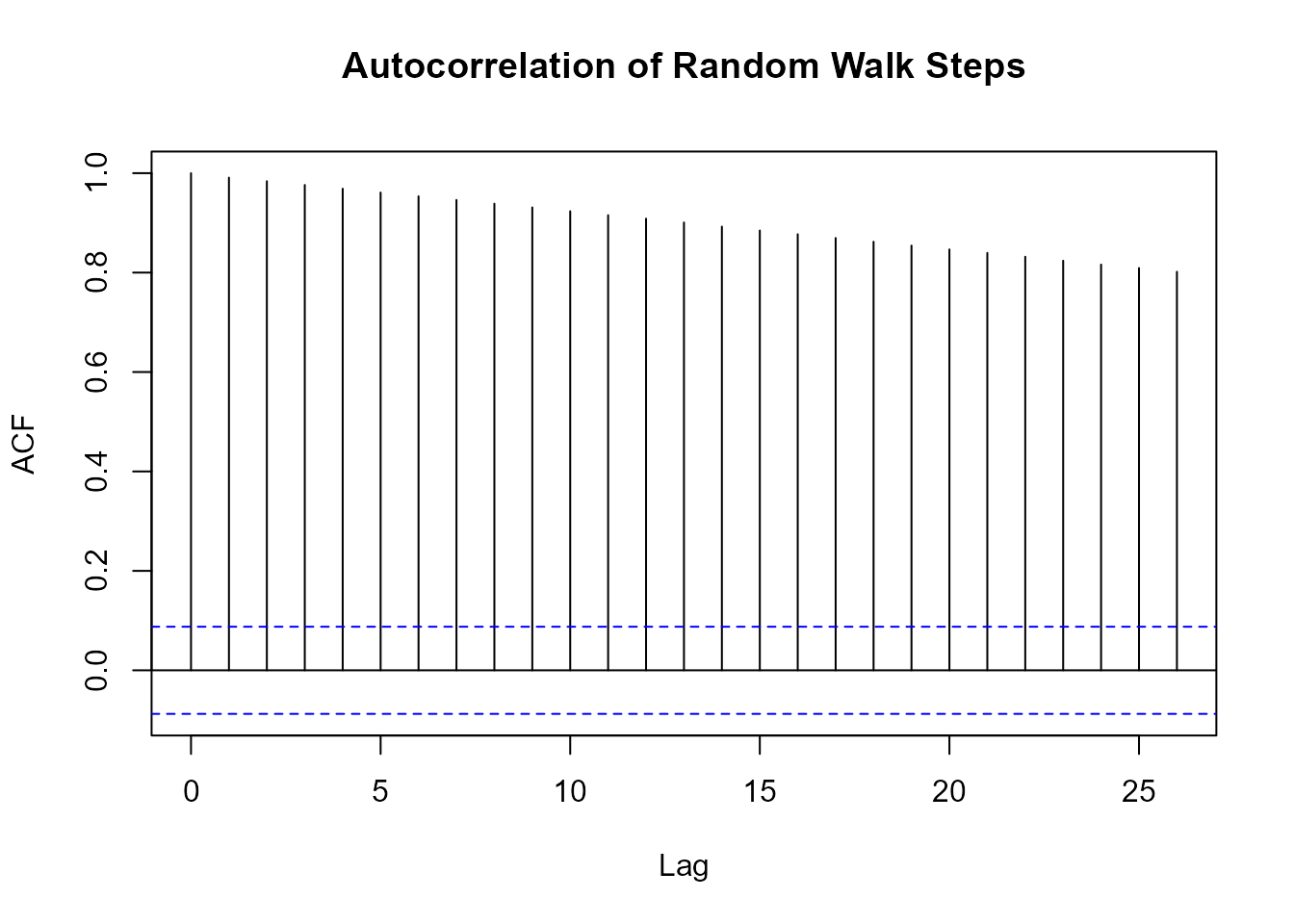

# Generate walk with drift

walks <- random_normal_drift_walk(.num_walks = 1, .n = 500, .mu = 0.1)

# Calculate autocorrelation

acf_result <- walks |> pull(y) |> acf(plot = FALSE)

# Plot

plot(acf_result, main = "Autocorrelation of Random Walk Steps")

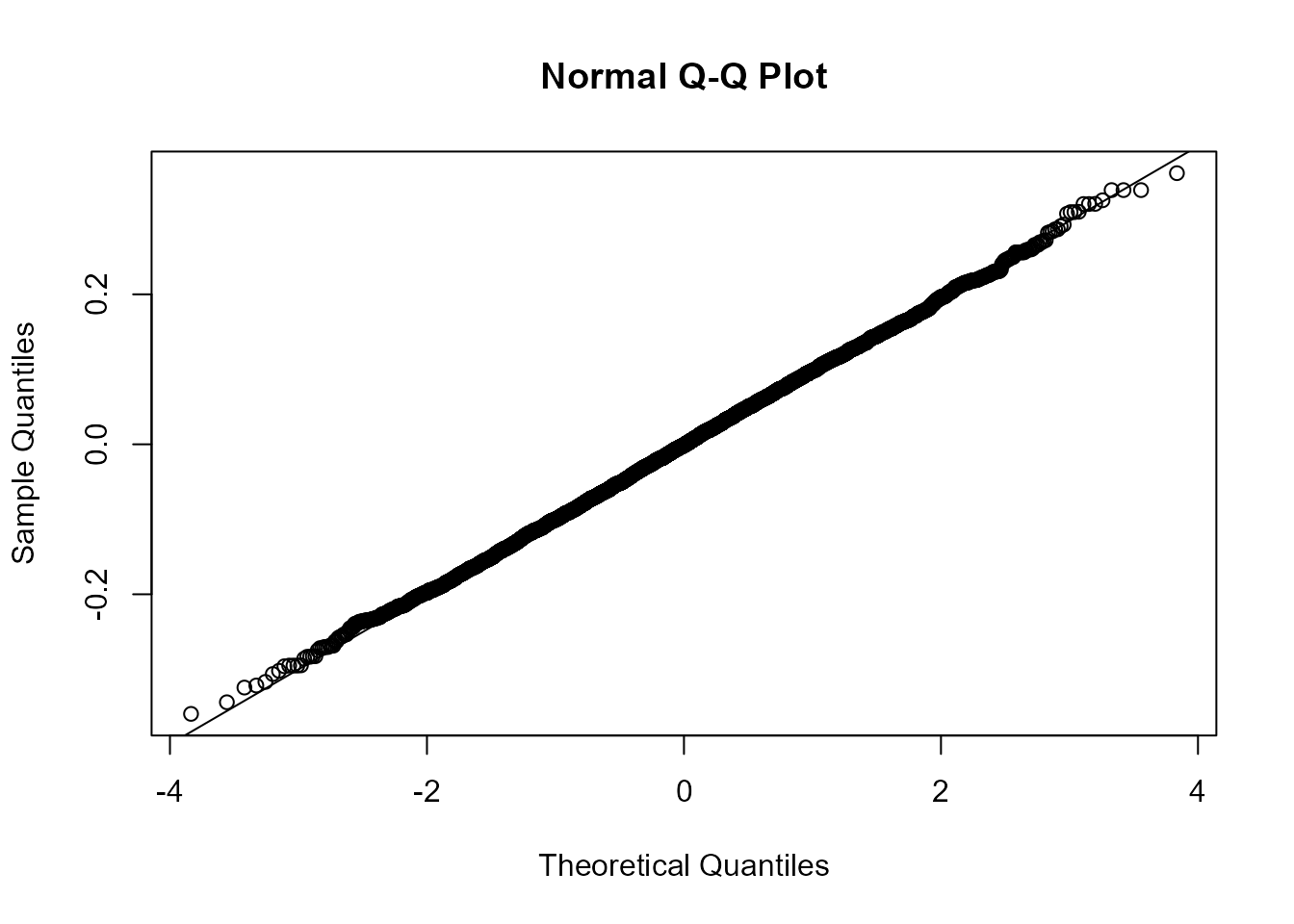

Distribution Testing

# Generate walks

walks <- random_normal_walk(.num_walks = 100, .n = 100)

# Test if steps are normally distributed

steps <- walks |> pull(y)

# Shapiro-Wilk test for normality

shapiro.test(sample(steps, 5000)) # Sample for computational efficiency

#>

#> Shapiro-Wilk normality test

#>

#> data: sample(steps, 5000)

#> W = 0.99943, p-value = 0.1313

# Q-Q plot

qqnorm(steps)

qqline(steps)

Variance Ratio Test

Test for random walk hypothesis:

# Generate walk

walk <- random_normal_walk(.num_walks = 1, .n = 1000)

# Calculate variance ratio

values <- walk |> pull(cum_sum_y)

# Variance of k-differences

k <- 10

var_k <- var(diff(values, lag = k))

var_1 <- var(diff(values, lag = 1))

# Variance ratio (should be ≈ k for random walk)

vr <- var_k / (k * var_1)

print(paste("Variance Ratio:", round(vr, 3), "| Expected:", k))

#> [1] "Variance Ratio: 1.014 | Expected: 10"Return Analysis (Financial)

# Generate stock price simulation

prices <- geometric_brownian_motion(

.num_walks = 1,

.n = 252,

.mu = 0.08,

.sigma = 0.25,

.initial_value = 100

)

# Calculate returns

returns <- prices |>

mutate(

log_return = log(cum_prod_y / lag(cum_prod_y)),

simple_return = (cum_prod_y - lag(cum_prod_y)) / lag(cum_prod_y)

) |>

filter(!is.na(log_return))

# Analyze returns

returns |>

summarize(

mean_return = mean(log_return) * 252, # Annualized

volatility = sd(log_return) * sqrt(252), # Annualized

sharpe_ratio = mean_return / volatility

)

#> # A tibble: 1 × 3

#> mean_return volatility sharpe_ratio

#> <dbl> <dbl> <dbl>

#> 1 144. 0.928 155.Statistical Tests

Comparing Distributions

# Generate two types of walks

normal_walks <- random_normal_walk(.num_walks = 50, .n = 100)

cauchy_walks <- random_cauchy_walk(.num_walks = 50, .n = 100)

# Get final values

normal_final <- normal_walks |>

group_by(walk_number) |>

slice_max(step_number) |>

pull(cum_sum_y)

cauchy_final <- cauchy_walks |>

group_by(walk_number) |>

slice_max(step_number) |>

pull(cum_sum_y)

# Wilcoxon rank-sum test (non-parametric)

wilcox.test(normal_final, cauchy_final)

#>

#> Wilcoxon rank sum test with continuity correction

#>

#> data: normal_final and cauchy_final

#> W = 1266, p-value = 0.9149

#> alternative hypothesis: true location shift is not equal to 0

# Kolmogorov-Smirnov test

ks.test(normal_final, cauchy_final)

#>

#> Exact two-sample Kolmogorov-Smirnov test

#>

#> data: normal_final and cauchy_final

#> D = 0.48, p-value = 1.387e-05

#> alternative hypothesis: two-sidedTesting for Drift

# Generate walk with known drift

walks <- random_normal_drift_walk(.num_walks = 100, .n = 100, .mu = 0.1)

# Test if mean step is significantly different from 0

steps <- walks |> pull(y)

t.test(steps, mu = 0)

#>

#> One Sample t-test

#>

#> data: steps

#> t = 115.67, df = 9999, p-value < 2.2e-16

#> alternative hypothesis: true mean is not equal to 0

#> 95 percent confidence interval:

#> 10.10977 10.45834

#> sample estimates:

#> mean of x

#> 10.28405Next Steps

- Visualization Guide - Visualize your analysis

- Use Cases and Examples - Real-world applications

- Multi-Dimensional Walks - Analyze spatial walks

- API Reference - Complete function documentation

Need more examples? Check out the Use Cases and Examples vignette for more real-world applications!