Real-world examples demonstrating TidyDensity in action across various domains and applications.

Data Science and Analytics

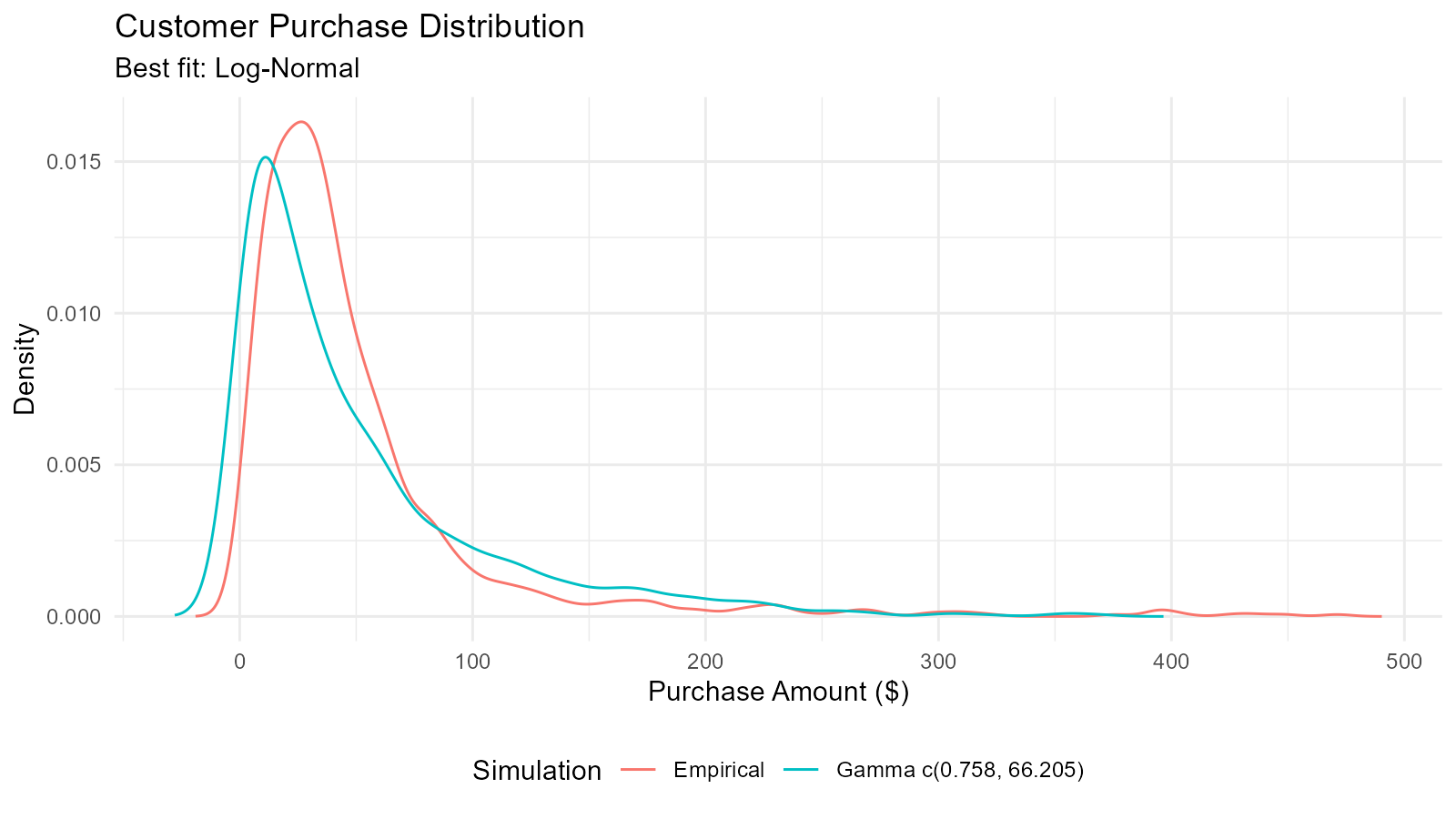

Example 1: Exploring Customer Purchase Amounts

# Simulate customer purchase data

purchases <- c(rgamma(800, shape = 2, rate = 0.05), # Regular customers

rexp(200, rate = 0.01)) # Big spenders

# Fit multiple distributions

normal_fit <- util_normal_param_estimate(purchases, .auto_gen_empirical = TRUE)

gamma_fit <- util_gamma_param_estimate(purchases, .auto_gen_empirical = TRUE)

lognormal_fit <- util_lognormal_param_estimate(purchases, .auto_gen_empirical = TRUE)

# Compare using AIC

aic_comparison <- data.frame(

Distribution = c("Normal", "Gamma", "Log-Normal"),

AIC = c(

util_normal_aic(.x = purchases),

util_gamma_aic(.x = purchases),

util_lognormal_aic(.x = purchases)

)

)

# Best distribution

best_dist <- aic_comparison[which.min(aic_comparison$AIC), ]

print(paste("Best fitting distribution:", best_dist$Distribution))

#> [1] "Best fitting distribution: Log-Normal"

# Visualize best fit

gamma_fit$combined_data_tbl |>

tidy_combined_autoplot() +

labs(title = "Customer Purchase Distribution",

subtitle = paste("Best fit:", best_dist$Distribution),

x = "Purchase Amount ($)",

y = "Density")

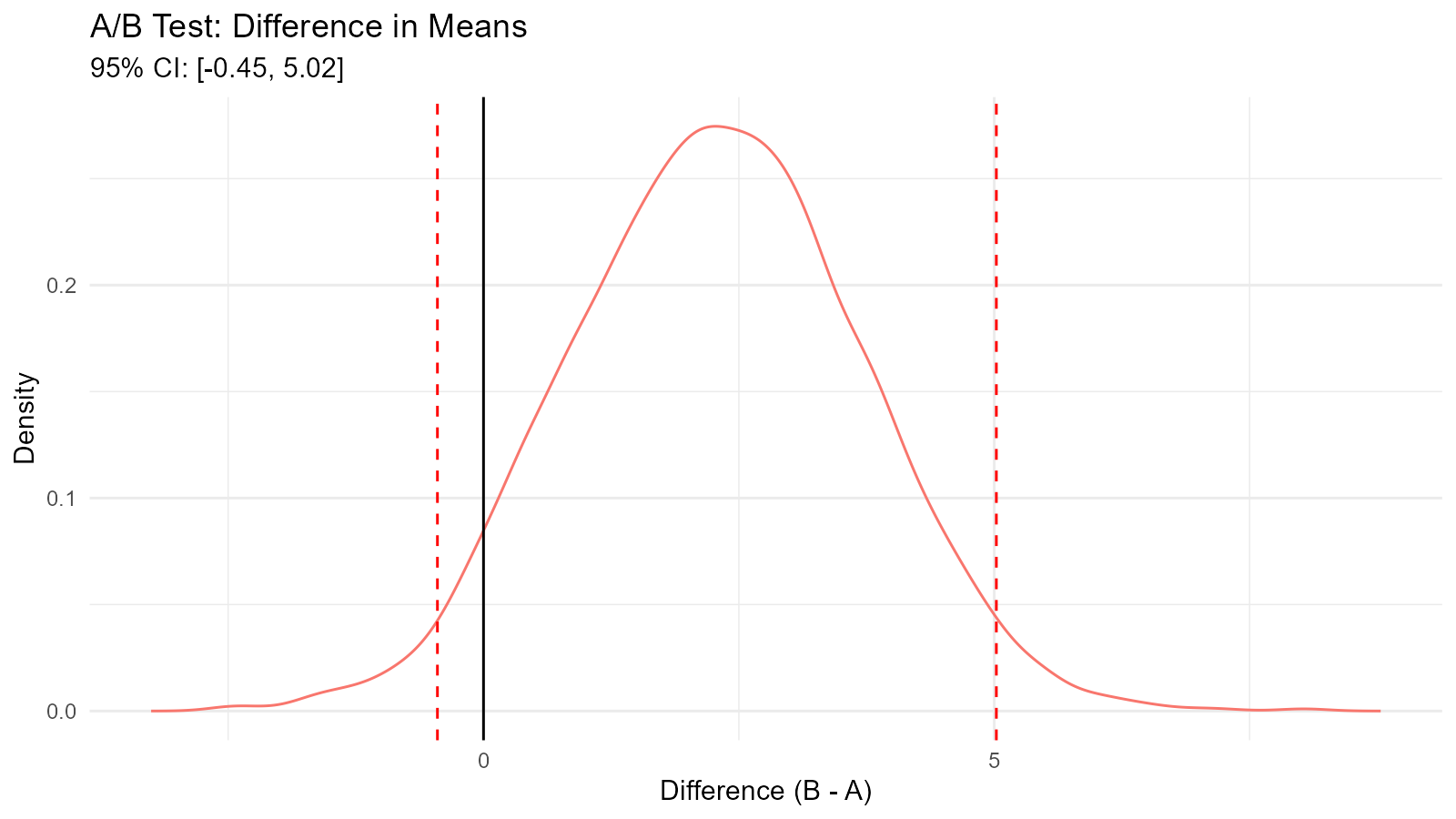

Example 2: A/B Test Analysis with Bootstrap

# Simulate A/B test data

group_a <- rnorm(100, mean = 50, sd = 10) # Control

group_b <- rnorm(100, mean = 55, sd = 10) # Treatment

# Bootstrap confidence intervals

bootstrap_diff <- function(n_sims = 5000) {

diffs <- numeric(n_sims)

for (i in 1:n_sims) {

boot_a <- sample(group_a, length(group_a), replace = TRUE)

boot_b <- sample(group_b, length(group_b), replace = TRUE)

diffs[i] <- mean(boot_b) - mean(boot_a)

}

return(diffs)

}

# Run bootstrap

diff_distribution <- bootstrap_diff(5000)

# Calculate CI

ci <- quantile(diff_distribution, c(0.025, 0.975))

mean_diff <- mean(diff_distribution)

# Visualize

boot_tbl <- tidy_empirical(.x = diff_distribution, .num_sims = 1)

tidy_autoplot(boot_tbl, .plot_type = "density") +

geom_vline(xintercept = ci[1], linetype = "dashed", color = "red") +

geom_vline(xintercept = ci[2], linetype = "dashed", color = "red") +

geom_vline(xintercept = 0, linetype = "solid", color = "black") +

labs(title = "A/B Test: Difference in Means",

subtitle = sprintf("95%% CI: [%.2f, %.2f]", ci[1], ci[2]),

x = "Difference (B - A)",

y = "Density")

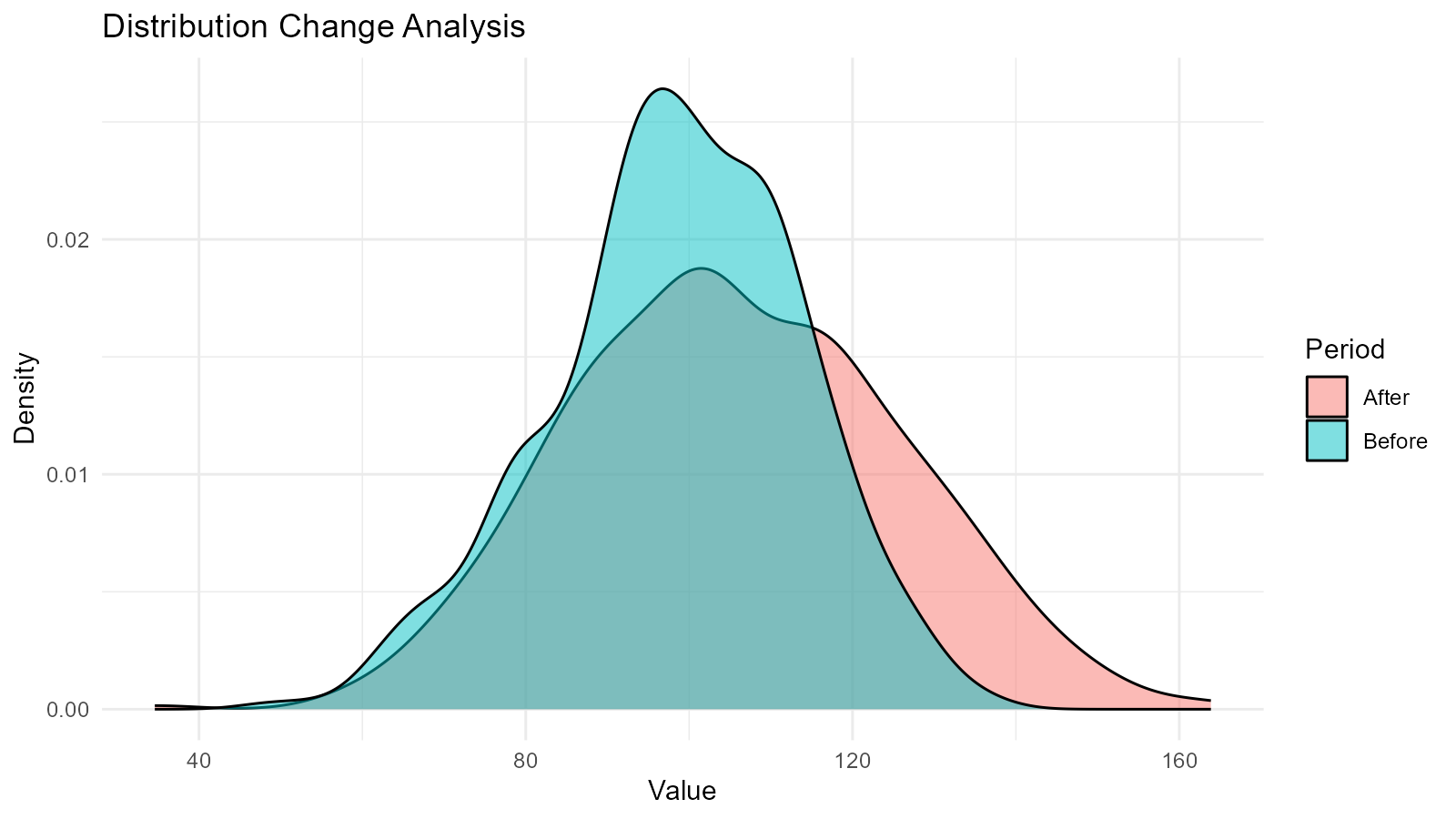

Example 3: Detecting Data Distribution Changes

# Before and after data

before <- rnorm(500, mean = 100, sd = 15)

after <- rnorm(500, mean = 105, sd = 20) # Mean shift and more variance

# Generate distributions

dist_before <- tidy_empirical(.x = before, .num_sims = 1)

dist_after <- tidy_empirical(.x = after, .num_sims = 1)

# Combine for visualization

combined <- bind_rows(

dist_before |> mutate(period = "Before"),

dist_after |> mutate(period = "After")

)

# Plot

ggplot(combined, aes(x = y, fill = period)) +

geom_density(alpha = 0.5) +

labs(title = "Distribution Change Analysis",

x = "Value",

y = "Density",

fill = "Period") +

theme_minimal()

# Statistical comparison

cat("Before: Mean =", round(mean(before), 2), ", SD =", round(sd(before), 2), "\n")

#> Before: Mean = 98.48 , SD = 15.2

cat("After: Mean =", round(mean(after), 2), ", SD =", round(sd(after), 2), "\n")

#> After: Mean = 105.61 , SD = 20.05

# Test for difference

t_test_result <- t.test(after, before)

cat("T-test p-value:", t_test_result$p.value, "\n")

#> T-test p-value: 3.793033e-10Statistical Analysis

Example 4: Power Analysis for Sample Size Determination

# Simulate power analysis

effect_sizes <- seq(0.2, 1.0, by = 0.1)

sample_sizes <- seq(30, 200, by = 10)

power_results <- expand.grid(effect_size = effect_sizes,

sample_size = sample_sizes)

# Calculate power for each combination

calculate_power <- function(n, effect) {

simulations <- 1000

significant <- 0

for (i in 1:simulations) {

group1 <- rnorm(n, mean = 0, sd = 1)

group2 <- rnorm(n, mean = effect, sd = 1)

p_value <- t.test(group1, group2)$p.value

if (p_value < 0.05) significant <- significant + 1

}

return(significant / simulations)

}

# Run for a few key combinations (subset for speed)

key_combos <- power_results[c(1, 50, 100, 150), ] |> na.omit()

key_combos$power <- mapply(calculate_power,

key_combos$sample_size,

key_combos$effect_size)

print(key_combos)

#> effect_size sample_size power

#> 1 0.2 30 0.119

#> 50 0.6 80 0.968

#> 100 0.2 140 0.389

#> 150 0.7 190 1.000Example 5: Distribution Goodness-of-Fit Testing

# Generate data (actually from gamma, but test multiple)

test_data <- rgamma(200, shape = 3, rate = 0.5)

# Fit multiple distributions and test

distributions <- list(

"Normal" = function(x) util_normal_param_estimate(x, .auto_gen_empirical = FALSE),

"Gamma" = function(x) util_gamma_param_estimate(x, .auto_gen_empirical = FALSE),

"Weibull" = function(x) util_weibull_param_estimate(x, .auto_gen_empirical = FALSE),

"Log-Normal" = function(x) util_lognormal_param_estimate(x, .auto_gen_empirical = FALSE)

)

# Calculate AIC for each

aic_results <- c(

"Normal" = util_normal_aic(.x = test_data),

"Gamma" = util_gamma_aic(.x = test_data),

"Weibull" = util_weibull_aic(.x = test_data),

"Log-Normal" = util_lognormal_aic(.x = test_data)

)

# Results

results_df <- data.frame(

Distribution = names(aic_results),

AIC = aic_results,

Delta_AIC = aic_results - min(aic_results)

) |>

arrange(AIC)

print(results_df)

#> Distribution AIC Delta_AIC

#> Gamma Gamma 1009.000 0.000000

#> Log-Normal Log-Normal 1013.549 4.549198

#> Weibull Weibull 1023.253 14.253167

#> Normal Normal 1082.418 73.417824

cat("\nBest fitting distribution:", results_df$Distribution[1], "\n")

#>

#> Best fitting distribution: GammaFinance and Risk Management

Example 6: Value at Risk (VaR) Calculation

# Simulate daily returns

returns <- rnorm(1000, mean = 0.001, sd = 0.02) # 0.1% daily return, 2% volatility

# Create distribution

returns_dist <- tidy_empirical(.x = returns, .num_sims = 1)

# Calculate VaR at different confidence levels

var_95 <- quantile(returns, 0.05)

var_99 <- quantile(returns, 0.01)

var_995 <- quantile(returns, 0.005)

# Bootstrap for VaR confidence intervals

boot_returns <- tidy_bootstrap(.x = returns, .num_sims = 2000)

boot_var <- boot_returns |>

bootstrap_unnest_tbl() |>

group_by(sim_number) |>

summarise(var_95 = quantile(y, 0.05)) |>

ungroup()

var_ci <- quantile(boot_var$var_95, c(0.025, 0.975))

# Results

cat("Value at Risk (VaR) Analysis\n")

#> Value at Risk (VaR) Analysis

cat("95% VaR:", round(var_95 * 100, 3), "%\n")

#> 95% VaR: -3.199 %

cat("99% VaR:", round(var_99 * 100, 3), "%\n")

#> 99% VaR: -4.479 %

cat("99.5% VaR:", round(var_995 * 100, 3), "%\n")

#> 99.5% VaR: -5.064 %

cat("\n95% CI for 95% VaR: [", round(var_ci[1] * 100, 3), "%,",

round(var_ci[2] * 100, 3), "%]\n")

#>

#> 95% CI for 95% VaR: [ -3.386 %, -2.958 %]

# Visualize

tidy_autoplot(returns_dist, .plot_type = "density") +

geom_vline(xintercept = var_95, color = "orange", linetype = "dashed") +

geom_vline(xintercept = var_99, color = "red", linetype = "dashed") +

annotate("text", x = var_95, y = 0, label = "95% VaR", vjust = -1) +

annotate("text", x = var_99, y = 0, label = "99% VaR", vjust = -1) +

labs(title = "Portfolio Returns Distribution with VaR",

x = "Daily Return",

y = "Density")

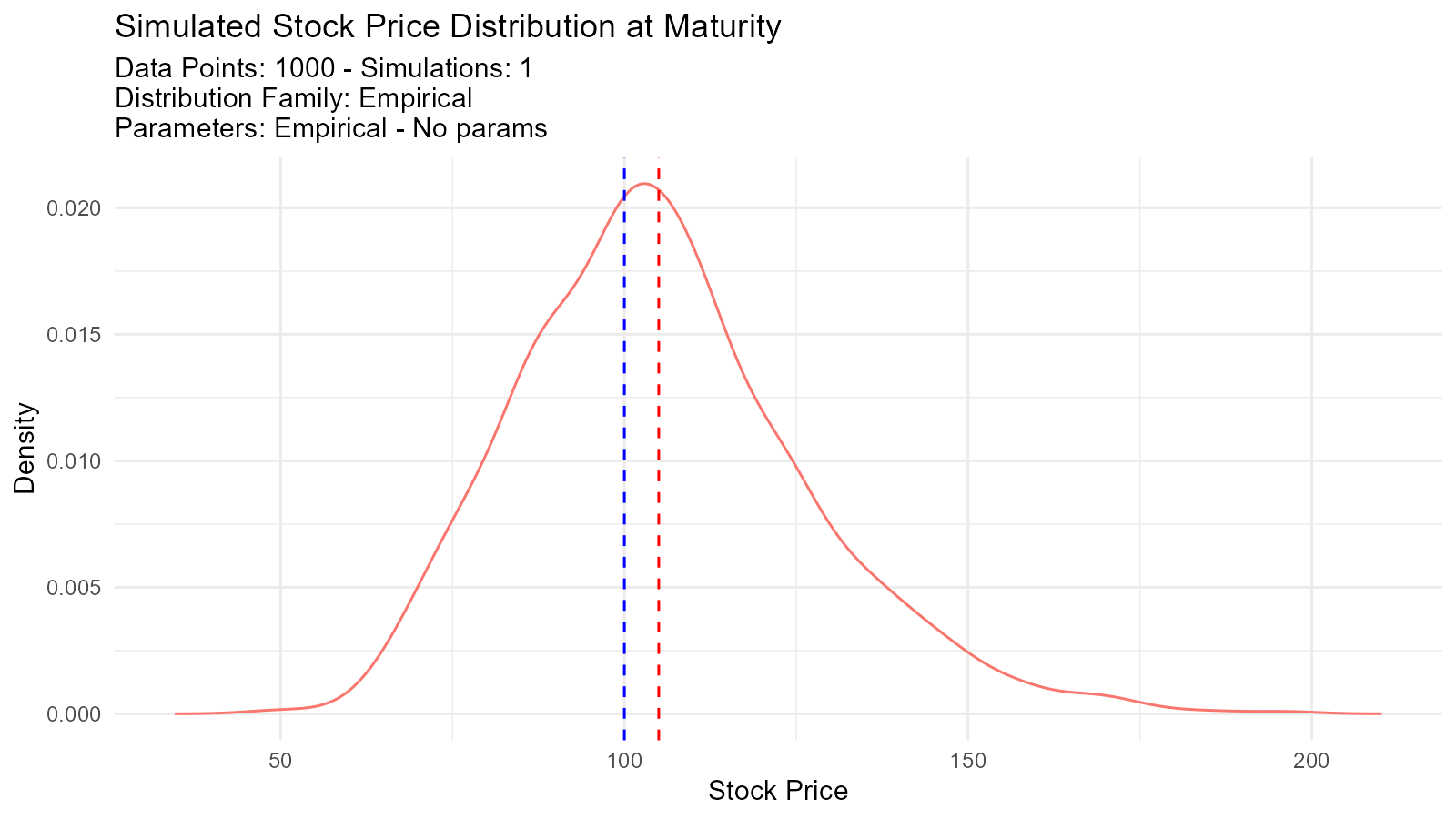

Example 7: Option Pricing with Monte Carlo Simulation

# Simulate stock price paths using GBM

stock_price_simulation <- function(S0, mu, sigma, T, n_steps, n_sims) {

dt <- T / n_steps

paths <- matrix(0, nrow = n_steps + 1, ncol = n_sims)

paths[1, ] <- S0

for (i in 2:(n_steps + 1)) {

Z <- rnorm(n_sims)

paths[i, ] <- paths[i-1, ] * exp((mu - 0.5 * sigma^2) * dt + sigma * sqrt(dt) * Z)

}

return(paths)

}

# Parameters

S0 <- 100 # Initial stock price

K <- 105 # Strike price

mu <- 0.05 # Drift

sigma <- 0.2 # Volatility

T <- 1 # Time to maturity (1 year)

n_steps <- 252 # Daily steps

n_sims <- 1000

# Simulate

paths <- stock_price_simulation(S0, mu, sigma, T, n_steps, n_sims)

# Final prices

final_prices <- paths[nrow(paths), ]

# Option payoffs

call_payoffs <- pmax(final_prices - K, 0)

put_payoffs <- pmax(K - final_prices, 0)

# Expected values (discounted)

r <- 0.03 # Risk-free rate

call_price <- mean(call_payoffs) * exp(-r * T)

put_price <- mean(put_payoffs) * exp(-r * T)

cat("Call Option Price:", round(call_price, 2), "\n")

#> Call Option Price: 8.12

cat("Put Option Price:", round(put_price, 2), "\n")

#> Put Option Price: 7.74

# Visualize final price distribution

final_dist <- tidy_empirical(.x = final_prices, .num_sims = 1)

tidy_autoplot(final_dist, .plot_type = "density") +

geom_vline(xintercept = K, color = "red", linetype = "dashed") +

geom_vline(xintercept = S0, color = "blue", linetype = "dashed") +

labs(title = "Simulated Stock Price Distribution at Maturity",

x = "Stock Price",

y = "Density")

Quality Control and Manufacturing

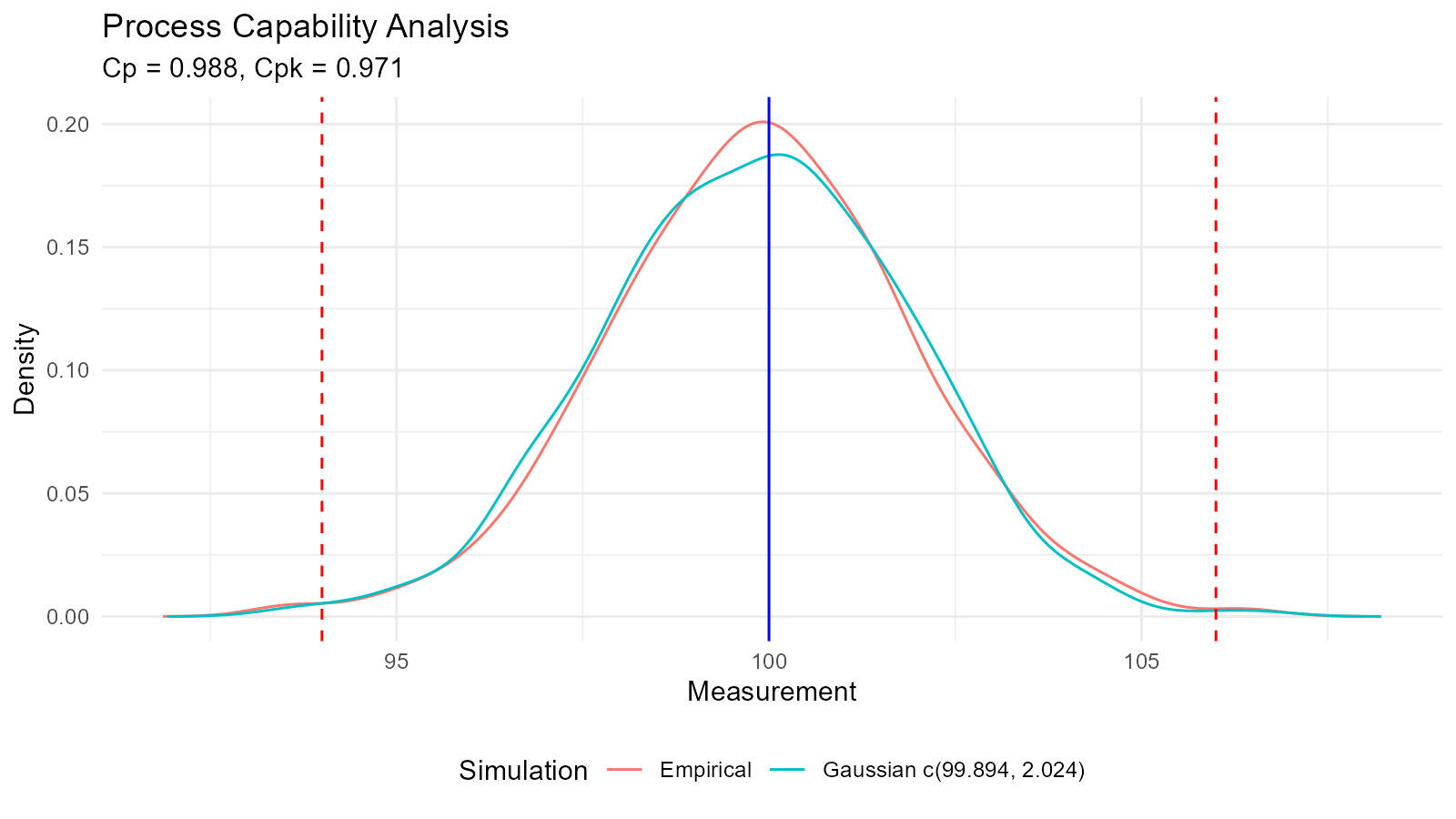

Example 8: Process Capability Analysis

# Manufacturing process data

measurements <- rnorm(500, mean = 100, sd = 2) # Target = 100

LSL <- 94 # Lower specification limit

USL <- 106 # Upper specification limit

# Fit distribution

fit <- util_normal_param_estimate(measurements, .auto_gen_empirical = TRUE)

mean_est <- fit$parameter_tbl$mu[1]

sd_est <- fit$parameter_tbl$stan_dev[1]

# Calculate Cp and Cpk

Cp <- (USL - LSL) / (6 * sd_est)

Cpu <- (USL - mean_est) / (3 * sd_est)

Cpl <- (mean_est - LSL) / (3 * sd_est)

Cpk <- min(Cpu, Cpl)

# Defect rate

defect_rate <- (pnorm(LSL, mean_est, sd_est) +

(1 - pnorm(USL, mean_est, sd_est))) * 100

# Results

cat("Process Capability Analysis\n")

#> Process Capability Analysis

cat("Cp:", round(Cp, 3), "\n")

#> Cp: 0.988

cat("Cpk:", round(Cpk, 3), "\n")

#> Cpk: 0.971

cat("Estimated Defect Rate:", round(defect_rate, 4), "%\n")

#> Estimated Defect Rate: 0.307 %

# Interpretation

if (Cpk >= 1.33) {

cat("Process capability: GOOD\n")

} else if (Cpk >= 1.0) {

cat("Process capability: ADEQUATE\n")

} else {

cat("Process capability: POOR - Action required\n")

}

#> Process capability: POOR - Action required

# Visualize

fit$combined_data_tbl |>

tidy_combined_autoplot() +

geom_vline(xintercept = LSL, color = "red", linetype = "dashed") +

geom_vline(xintercept = USL, color = "red", linetype = "dashed") +

geom_vline(xintercept = 100, color = "blue", linetype = "solid") +

labs(title = "Process Capability Analysis",

subtitle = sprintf("Cp = %.3f, Cpk = %.3f", Cp, Cpk),

x = "Measurement",

y = "Density")

Example 9: Control Chart Analysis

# Generate process data with a shift

n_before <- 200

n_after <- 50

before_shift <- rnorm(n_before, mean = 100, sd = 3)

after_shift <- rnorm(n_after, mean = 105, sd = 3) # Process shifted

all_data <- c(before_shift, after_shift)

time <- 1:length(all_data)

# Calculate control limits

mean_val <- mean(before_shift)

sd_val <- sd(before_shift)

UCL <- mean_val + 3 * sd_val

LCL <- mean_val - 3 * sd_val

# Create control chart

control_data <- data.frame(time = time, value = all_data)

ggplot(control_data, aes(x = time, y = value)) +

geom_line() +

geom_point() +

geom_hline(yintercept = mean_val, color = "blue") +

geom_hline(yintercept = UCL, color = "red", linetype = "dashed") +

geom_hline(yintercept = LCL, color = "red", linetype = "dashed") +

geom_vline(xintercept = n_before, color = "orange", linetype = "dotted") +

labs(title = "X-bar Control Chart",

subtitle = "Process Shift Detected",

x = "Sample",

y = "Measurement") +

theme_minimal()

Healthcare and Epidemiology

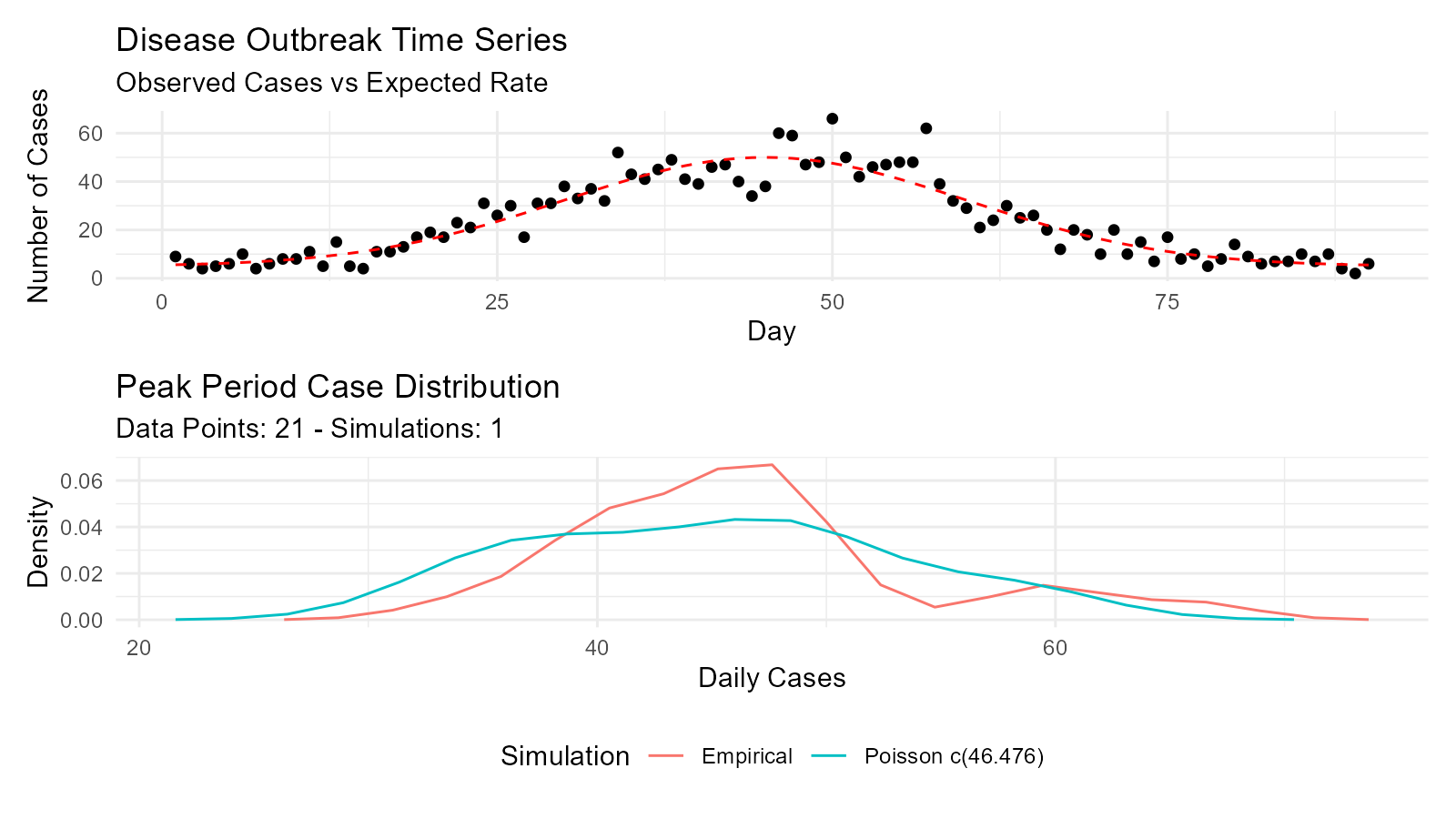

Example 10: Disease Outbreak Modeling

# Model daily case counts with Poisson distribution

days <- 1:90

baseline_rate <- 5

peak_rate <- 50

# Simulate outbreak with time-varying rate

lambda <- baseline_rate + (peak_rate - baseline_rate) *

exp(-((days - 45)^2) / (2 * 15^2)) # Gaussian curve

cases <- rpois(length(days), lambda)

# Fit Poisson distribution to peak period

peak_cases <- cases[35:55]

poisson_fit <- util_poisson_param_estimate(peak_cases, .auto_gen_empirical = TRUE)

# Visualize time series

outbreak_data <- data.frame(day = days, cases = cases, expected = lambda)

p1 <- ggplot(outbreak_data, aes(x = day, y = cases)) +

geom_point() +

geom_line(aes(y = expected), color = "red", linetype = "dashed") +

labs(title = "Disease Outbreak Time Series",

subtitle = "Observed Cases vs Expected Rate",

x = "Day",

y = "Number of Cases") +

theme_minimal()

# Peak analysis

p2 <- poisson_fit$combined_data_tbl |>

tidy_combined_autoplot() +

labs(title = "Peak Period Case Distribution",

x = "Daily Cases",

y = "Density")

p1 / p2

Machine Learning and Simulation

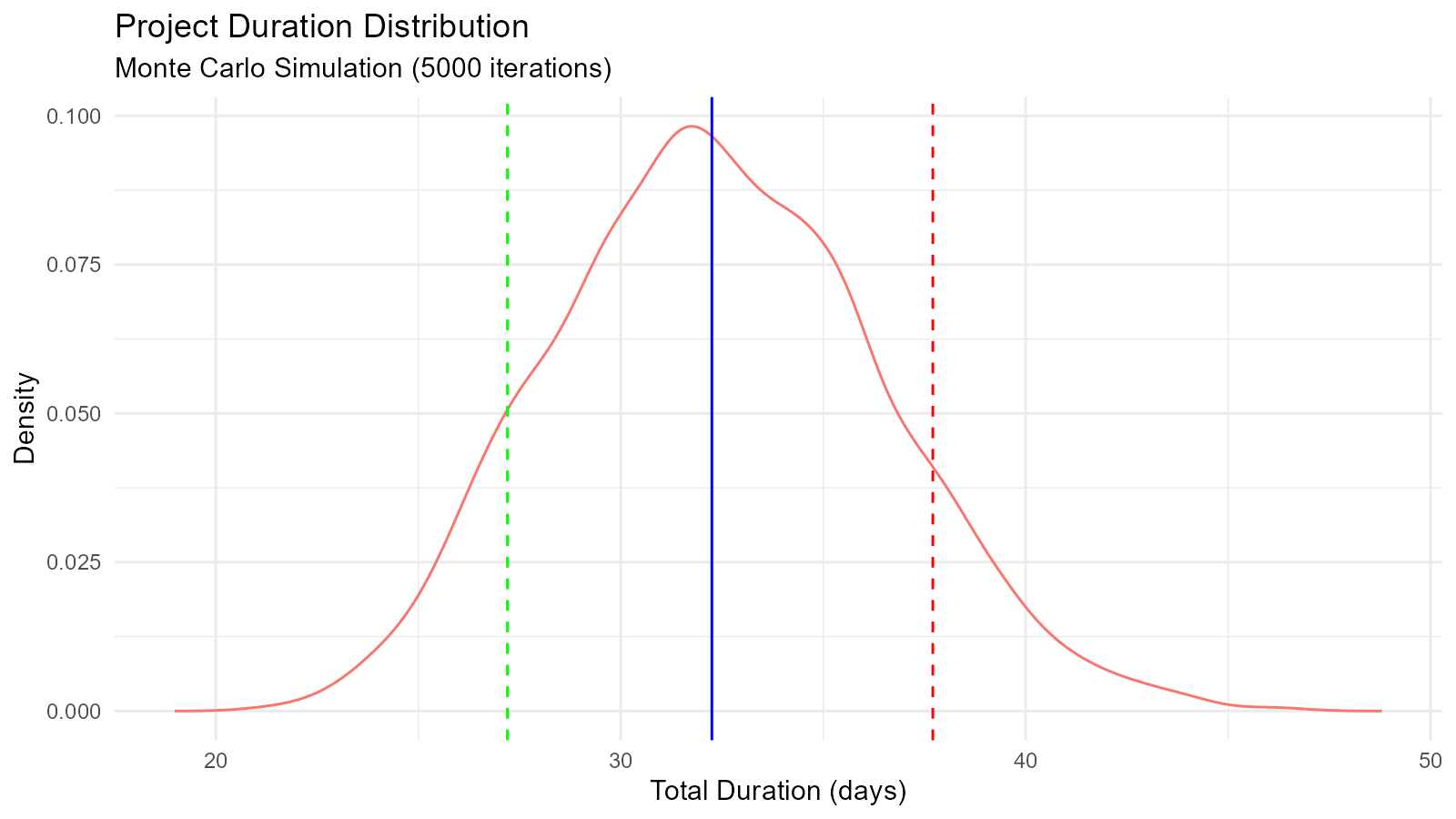

Example 11: Monte Carlo Simulation for Project Planning

# Project task duration simulation using triangular distribution

tasks <- list(

task1 = list(min = 5, mode = 8, max = 15),

task2 = list(min = 3, mode = 5, max = 10),

task3 = list(min = 7, mode = 10, max = 20),

task4 = list(min = 2, mode = 4, max = 8)

)

# Simulate total project duration

n_sims <- 5000

total_durations <- numeric(n_sims)

for (i in 1:n_sims) {

task_durations <- sapply(tasks, function(task) {

tidy_triangular(.n = 2, .min = task$min, .max = task$max, .mode = task$mode)$y[1]

})

total_durations[i] <- sum(task_durations)

}

# Analyze results

duration_dist <- tidy_empirical(.x = total_durations, .num_sims = 1)

percentiles <- quantile(total_durations, c(0.1, 0.5, 0.9))

cat("Project Duration Analysis\n")

#> Project Duration Analysis

cat("10th percentile (optimistic):", round(percentiles[1], 1), "days\n")

#> 10th percentile (optimistic): 27.2 days

cat("50th percentile (median):", round(percentiles[2], 1), "days\n")

#> 50th percentile (median): 32.3 days

cat("90th percentile (pessimistic):", round(percentiles[3], 1), "days\n")

#> 90th percentile (pessimistic): 37.7 days

# Visualize

tidy_autoplot(duration_dist, .plot_type = "density") +

geom_vline(xintercept = percentiles[1], color = "green", linetype = "dashed") +

geom_vline(xintercept = percentiles[2], color = "blue", linetype = "solid") +

geom_vline(xintercept = percentiles[3], color = "red", linetype = "dashed") +

labs(title = "Project Duration Distribution",

subtitle = "Monte Carlo Simulation (5000 iterations)",

x = "Total Duration (days)",

y = "Density")

Education and Teaching

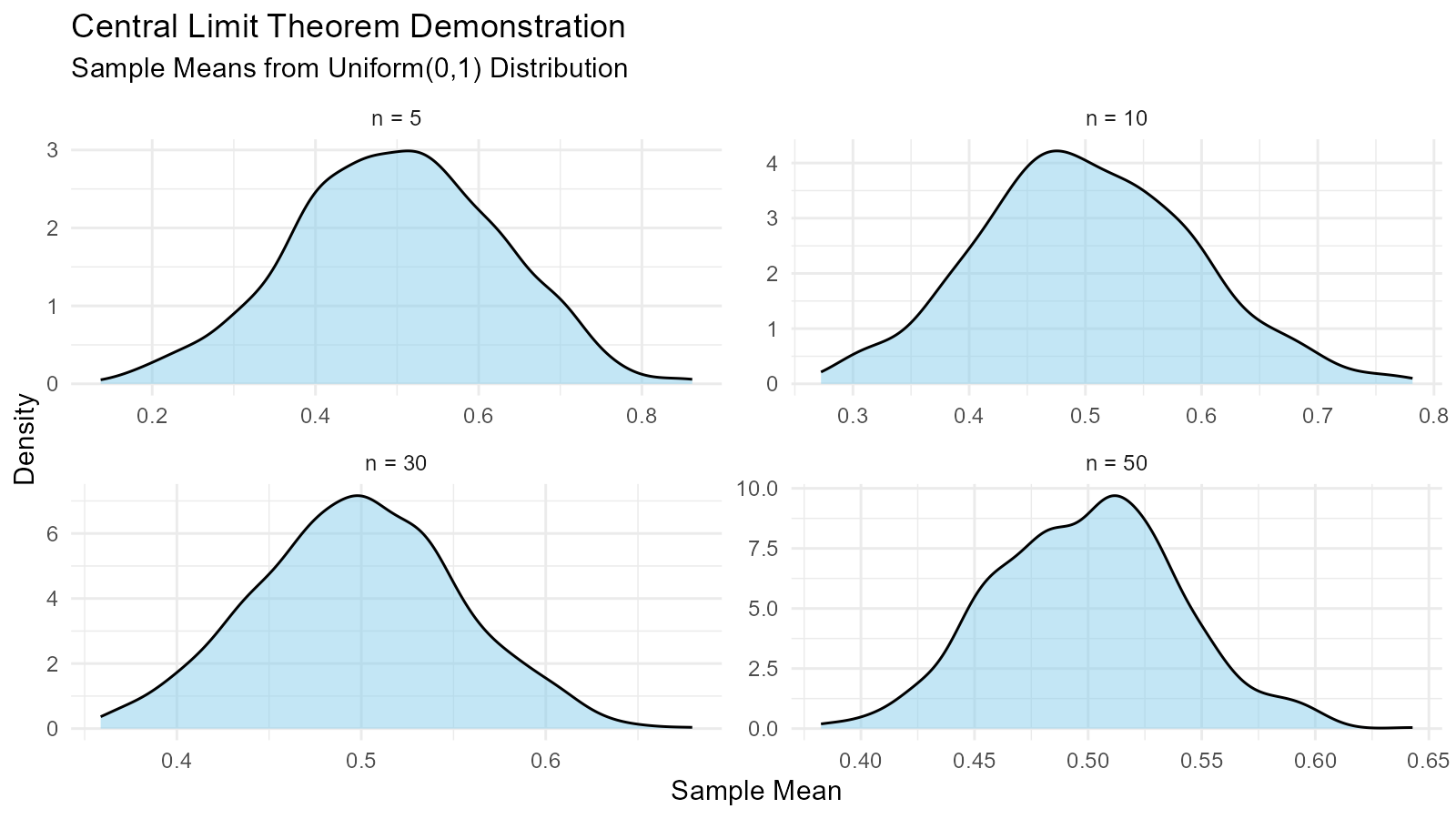

Example 12: Demonstrating Central Limit Theorem

# Show CLT with different source distributions

n_samples <- 1000

sample_sizes <- c(5, 10, 30, 50)

demonstrate_clt <- function(source_dist_func, sample_size, n_samples) {

sample_means <- numeric(n_samples)

for (i in 1:n_samples) {

sample <- source_dist_func(sample_size)

sample_means[i] <- mean(sample)

}

return(sample_means)

}

# Source: Uniform distribution

uniform_source <- function(n) runif(n, 0, 1)

# Generate for different sample sizes

results <- lapply(sample_sizes, function(n) {

means <- demonstrate_clt(uniform_source, n, n_samples)

tidy_empirical(.x = means, .num_sims = 1) |>

mutate(sample_size = n)

})

# Combine and plot

combined <- bind_rows(results)

ggplot(combined, aes(x = y)) +

geom_density(fill = "skyblue", alpha = 0.5) +

facet_wrap(~sample_size, scales = "free",

labeller = labeller(sample_size = function(x) paste("n =", x))) +

labs(title = "Central Limit Theorem Demonstration",

subtitle = "Sample Means from Uniform(0,1) Distribution",

x = "Sample Mean",

y = "Density") +

theme_minimal()

Tips for Your Own Use Cases

1. Start with Exploration

# Explore your data

summary(your_data)

hist(your_data)

# Try empirical distribution

emp <- tidy_empirical(.x = your_data, .num_sims = 1)

tidy_autoplot(emp, .plot_type = "density")3. Validate with Visualization

# Always visualize

fit <- get(paste0("util_", best, "_param_estimate"))(

your_data,

.auto_gen_empirical = TRUE

)

fit$combined_data_tbl |>

tidy_combined_autoplot()4. Use Bootstrap for Uncertainty

# Add bootstrap confidence intervals

boot <- tidy_bootstrap(.x = your_data, .num_sims = 2000)

boot |>

bootstrap_unnest_tbl() |>

summarise(

lower = quantile(y, 0.025),

upper = quantile(y, 0.975)

)Key Takeaways

1. Distribution Fitting is Essential

Use AIC to compare multiple candidate distributions and select the best fit for your data.

2. Bootstrap Provides Robust Uncertainty

When parametric assumptions are uncertain, bootstrap resampling gives reliable confidence intervals.

3. Visualization Validates Analysis

Always plot your results to verify that fitted distributions match the empirical data.